The Sol SOURCE is a monthly journal that our team distributes to our network of clients and solar stakeholders. Our newsletter contains energy statistics from current real-life renewables projects, trends, and observations gained through monthly interviews with our team, and it incorporates news from a variety of industry resources.

Below, we have included excerpts from the March 2017 edition. To receive future Journals, please subscribe or email pr@solsystems.com.

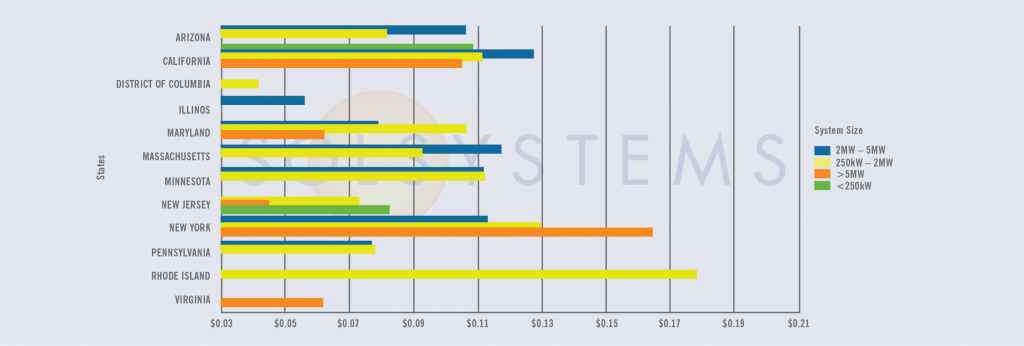

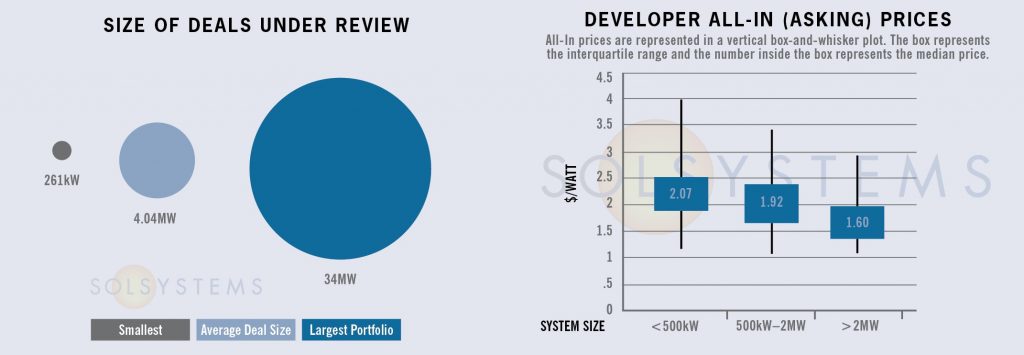

PROJECT FINANCE STATISTICS

The following statistics represent some high-quality solar projects and portfolios that we are actively reviewing for investment.

Have a solar project in need of financing? Our team can provide a pricing quote for you here.

STATE MARKETS

Massachusetts – Uncertainty persists in Massachusetts as the solar industry and interested customers await final guidelines on the SREC II extension, as well as more defined details on the SMART program. While we may have to wait until April for more clarity from the Massachusetts Department of Energy Resources (DOER) on SMART, the fact that we now know that there will be some SREC II extension is enough to pursue project opportunities that can meet mechanical completion deadlines by Q1 2018 – which is when the new program is set to begin. Because the SREC II program is more lucrative than SMART – and because color on pricing under SMART will not likely be available until Q3 2017 – we recommend that developers urge customers to move quickly to meet the SREC II deadline.

It is important to note that neither the SREC II extension nor SMART will lift the net metering cap; a cap lift requires legislative action. While private projects in National Grid have a waitlist, there is still plenty of room for private projects in NSTAR territory and for public projects across all utility territories.

Rhode Island –After passing a package of legislation last summer to bolster the Ocean State’s solar energy market, Rhode Island is ready to take clean energy deployment to the next level. On March 1, Governor Raimondo announced a new goal: 1GW of clean energy by 2020, ten times the amount of renewable energy that the state has today. Under Governor Raimondo’s leadership, Rhode Island continues to position itself as one of the nation’s next leaders in clean energy deployment, leading the way on many national issues, including property tax and permitting standardization. Property tax standardization – or a lack thereof – is a constant challenge in solar energy development; we are hopeful that Rhode Island will set a precedent for other states to follow.

In the near-term, the 2017 Renewable Energy Growth (RE Growth) program will be open for enrollment between April 17 and April 28. The legislature is also looking at legislation to expand RE Growth for another 10 years after 2019 at another 40MW per year.

New York – New York has seen a flurry of regulatory activity this past month. On February 22, the Public Service Commission issued its Clean Energy Standard (CES) Phase 1 Implementation Order. The CES Order green lights an April 2017 procurement of large-scale renewables, which will be similar to the state’s incumbent Main Tier Renewable Portfolio Standards (RPS) solicitation with a few modifications. Under the Procurement, solar will complete with other Tier 1 sources for 20-year REC contracts.

On the distributed generation side, the Megawatt Block program for commercial and industrial (C&I) solar continues to experience challenges. While blocks continue to fill – we are now on block 9 out of 11 – much of the capacity that is filling the blocks is not being built either due to attrition, inability to meet required deadlines, system size changes, or other challenges. To account for this, NYSERDA adds the uncommitted megawatts to the open MW block at the time. However, this will unfortunately mean that the “clogging” happening at earlier blocks will push the more “real” projects to try and pencil under the lower incentive levels in the later blocks. According to the latest Solar Market Insight report, only 309MW of non-residential solar has been built in NY; the MW Block queue shows 1.1GW. NYSERDA recognizes these issues and will work over the next few months to address them. Interconnection queue reform continues to move forward as well, and could also affect megawatt allocations in the various blocks.

The Value of Distributed Energy Resources (VDER) was also released. The VDER order is nearly 300 pages full o’ fun, but in sum, will start the transition away from net energy metering (NEM) toward a “value stack” approach, valuing energy, capacity, the environmental value, and demand reduction and locational system relief value. Residential customers’ rates will be preserved until 2020. All other projects have 90 days to demonstrate that 25% of interconnection costs have been paid or a standard interconnection contract has been executed to get NEM with slight modifications. After that, we'll await an order on implementing the value stack "as soon as" this summer.

New York’s goals have been ambitious, and without a doubt, there are many lessons learned as new markets – such as Illinois – look at large-scale renewable energy procurements, declining block incentives, and locational based valuation of distributed energy resources.

SOLAR CHATTER

- This is a public service announcement about RECtirement. Our research has discovered a number of RECs in PJM-GATS and other registries that should be used for corporate claims and voluntary compliance, but are hanging in limbo instead of heading toward retirement. This makes true REC forecasting hazy and distorts supply and demand projections. As REC prices fall to single-digit levels, hitting the retirement button could go a long way in painting a clearer picture. Please spread the word around the corporate buyers’ water cooler, and we thank you in advance for your service.

- After a defeat in 2016, the Ohio legislature is trying yet again roll back its modest 12.5% renewable portfolio standard. Last year, more than 135 witnesses testified against similar legislation, and the Governor ultimately vetoed HB 544, noting that the roll back to the standards would have created “self-inflicted” damage to the state’s economic competitiveness. Governor Kasich has remained steadfast in his position, though the House version may still advance. While the legislature continues to look backward, the Public Utilities Commission of Ohio (PUCO) is looking ahead. The PUCO announced PowerForward, which will look at how Ohio can better incorporate modern technologies for grid of the future.

- The District of Columbia has announced $13M in grants for both residential and commercial-sized low-income solar projects. Given the District’s unique urban landscape, the District Department of Energy & the Environment (DOEE) will offer funding for projects that address key barriers to solar deployment in the District. These key barriers include real estate constraints (given the sheer size of the District of Columbia and availability of vacant rooftops), competition for rooftop space with the lucrative green roof rebate, acquiring low-income customers, and providing solar power benefits to low-income residents who do not receive electric bills.

- We are hearing that the latest iteration of LADWP’s feed-in tariff should be announced shortly. Stay tuned to the Sol SOURCE for updates.

- New England continues to be a hotbed for solar development, and not just in Massachusetts. We’ve covered Rhode Island extensively, and we are even starting to see pipeline in non-traditional Northeastern markets. On a related note, Connecticut is looking to extend its ZREC and LREC programs. While the extension will be a short-term fix (2 years), it could buy the state time to restructure its solar program to resemble that of Massachusetts or other successful programs. Smart move on the extension; as we have learned in Massachusetts, New York, and other states, restructuring a program takes time. While Connecticut has seen development as a result of the ZREC program, it remains relatively unpopular among developers given its stringent, expensive requirements for participation, such as the performance assurance requirement for winning bidders.

- What a year! SEIA/GTM released their Solar Market Insight 2016 Year in Review report earlier this month, showing a record-breaking 2016 for solar, as the industry installed 14,762MW of solar, almost doubling installed capacity for 2015.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered more than 500MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.