The Sol SOURCE is a monthly journal that our team distributes to our network of clients and solar stakeholders. Our newsletter contains energy statistics from current real-life renewables projects, trends, and observations gained through monthly interviews with our team, and it incorporates news from a variety of industry resources.

Below, we have included excerpts from the February 2017 edition. To receive future Journals, please subscribe or email pr@solsystems.com.

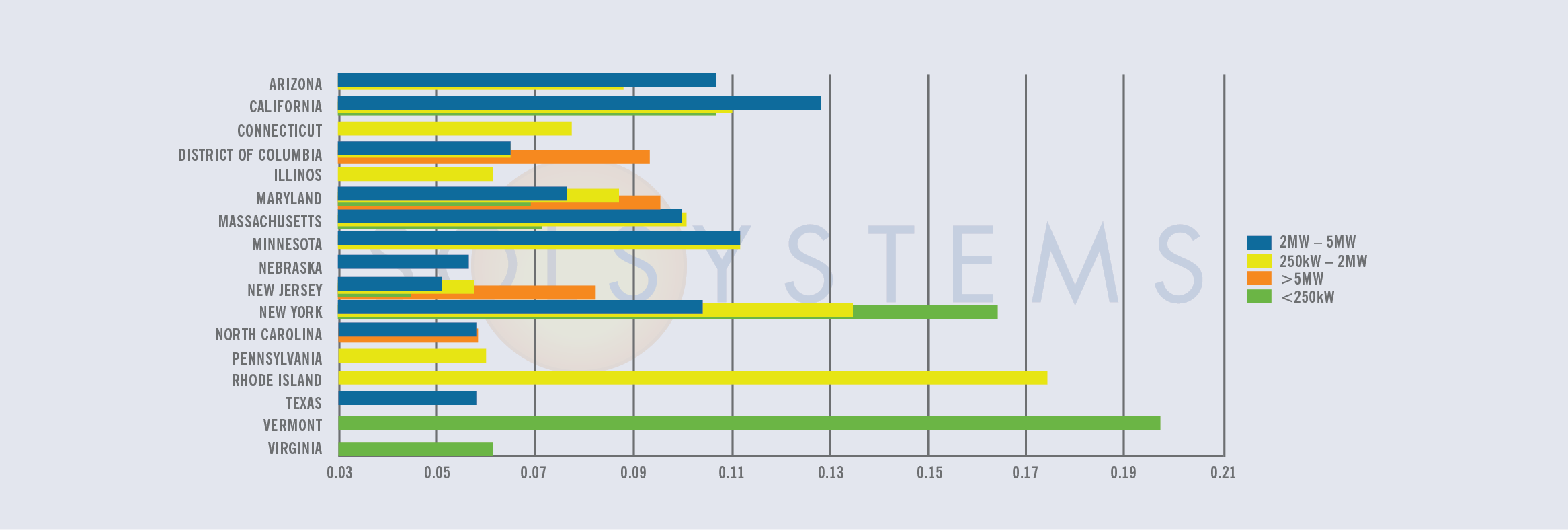

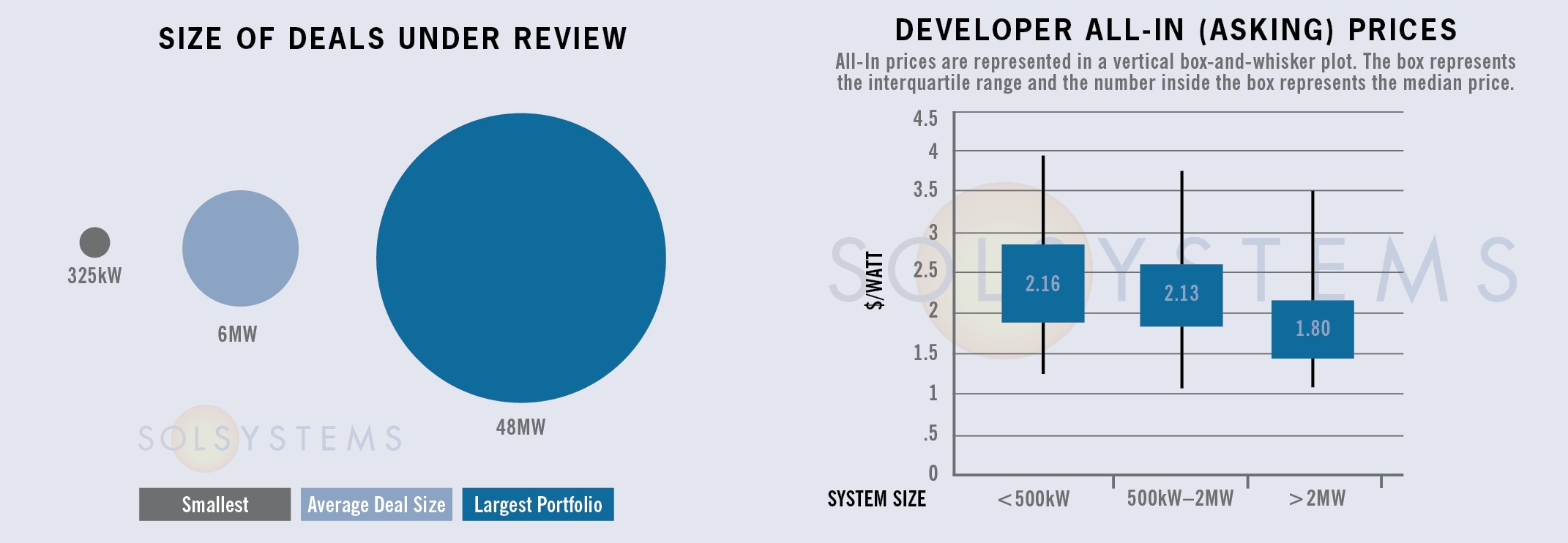

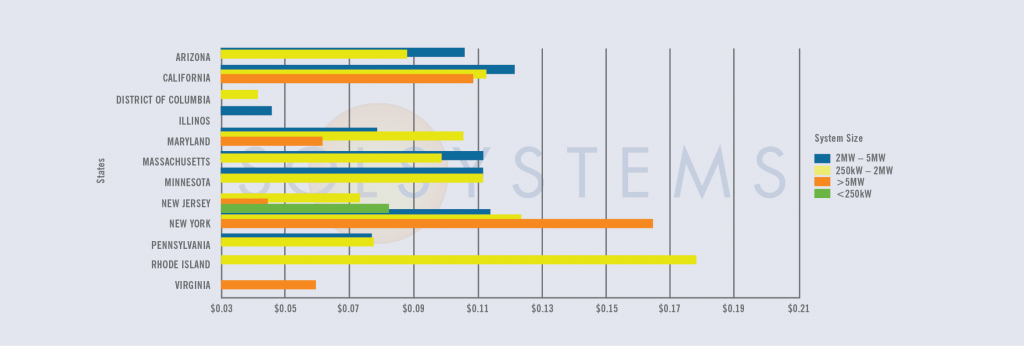

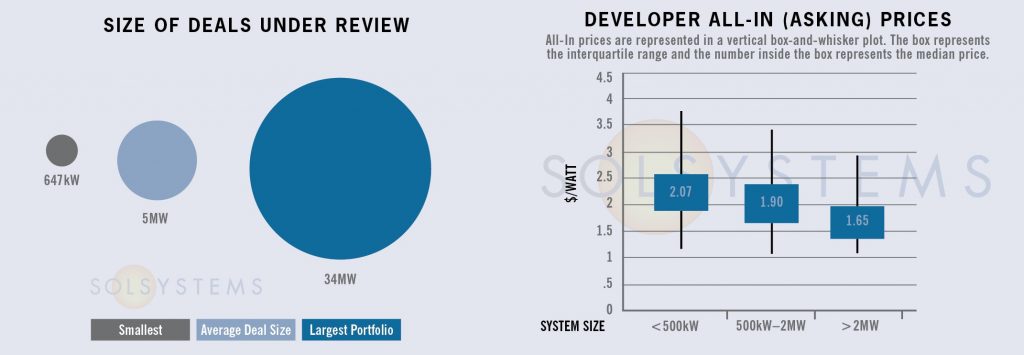

PROJECT FINANCE STATISTICS

The following statistics represent some high-quality solar projects and portfolios that we are actively reviewing for investment.

Have a solar project in need of financing? Our team can provide a pricing quote for you here.

STATE MARKETS

Maryland - It’s official. This month, the Maryland state legislature voted to override Governor Hogan’s veto to HB1106, the Clean Energy Jobs Act. With the override, the state’s renewable energy goal has increased to 25% by 2020 (up from 20% by 2022), and the solar carve-out increased from 2% by 2022 to 2.5% by 2020. While short-term SREC pricing did not increase, the override prevented a further dip in values. Its primary benefit will be a boost to 2019 and 2020 demand, which may result in higher pricing for those SREC vintages. Perhaps SREC prices will rise in coming years, but for now, $20/SREC is the new normal in Maryland, where SREC values have plummeted over the last year given rapid build, most notably of the residential sector. At press time, 493MW of behind-the-meter (<2MW) solar has been installed in Maryland, as compared to 171MW of projects over 2MW in size. More recently, two bills have been introduced to examine the oversupply in the SREC market: one that would expand the solar carve-out to 4% (HB1457) and another that would require a study to examine possible “bigger picture” changes to the RPS (HB1414).

Meanwhile, energy storage is a hot topic at the state legislature this session, where several storage bills will soon be heard in committee. Proposed legislation could create an energy storage income tax credit (HB0490/SB0758) and an energy storage grant program (HB1395). Introduced legislation would also require the Maryland Clean Energy Center to study possible incentives and regulatory constructs to encourage energy storage (HB0773/SB0715).

Massachusetts - After months of stakeholder engagement, the ever-patient, ever-diligent Massachusetts Department of Energy Resources (DOER) announced the design of Solar Massachusetts Renewable Target (SMART) program, the next iteration of the state’s solar incentive regime. As a refresher, commercial projects in the nation’s #7 solar market have come to a halt [with few exceptions] since the SREC II program closed. With SMART, Massachusetts will transition away from an SREC program and toward a declining block incentive. SMART will also incentivize rooftop solar, canopy structures, and storage – and provide a lower incentive to greenfield development. Land use and siting requirements will be more stringent than in SREC I and SREC II.

Transitioning from one program to the next takes time, and DOER acknowledged this at the January 31 "reveal". In order to avoid further disruptions in renewable energy investments in the Commonwealth (Massachusetts actually lost solar jobs this last year, according the latest Solar Jobs Census), the DOER will extend SREC II to provide a “bridge” to SMART. In order to qualify for SREC II at a discounted incentive level, projects must reach mechanical completion by the start of the new program, which is now estimated to begin in January 2018 at the earliest. These details are subject to change; comments on the SREC II extension were due February 17.

While SREC II has been extended, the net metering caps have not been lifted; legislation is required to lift the caps (again). The SMART program aims to circumvent this by providing developers with an “on-bill crediting” alternative to net metering. Notably, the Board of Public Utilities – not DOER – must lead this process and so there is a degree of uncertainty here. Details are still to be determined.

The Massachusetts market is experiencing many changes. Sol Systems is following the market transition closely and would be happy to talk them through with you. Feel free to give us a call at (202) 349-2085.

South Carolina - Solar incentive programs for non-residential projects up to 1MW AC in Duke Progress and Duke Carolinas territory have filled, and South Carolina Gas & Electric is soon to follow. While cumbersome fee in lieu of taxes (FILOT) negotiations have hindered economics for commercial and industrial solar projects in the Palmetto state, project economics could improve vastly if property tax abatement legislation is passed this year. The Renewable Energy Property Tax Act (S.44) passed its third and final reading in the Senate in early February and now sits with House Ways & Means. If passed, South Carolina would offer an 80% property tax abatement for non-residential systems, much like its neighbor to the North. Property tax abatement nearly passed last year, but failed after a last minute “poison pill.”

SOLAR CHATTER

- The numbers are in. The U.S. solar industry added more than 14.6 gigawatts of new capacity in 2016, a 95% increase over 2015! As of November 2016, the industry now employs over 260,000 solar workers across the country, up from 210,000 jobs in 2015. The Solar Foundation estimates that one out of every 50 new jobs added in the United States in 2016 was created by the solar industry, representing 2% percent of all new jobs. Can’t stop, won’t stop.

- Will the corporate offsite space move away from the RFP business model as more bilateral conversations between corporate purchases and developers pick up steam? We’re watching this trend closely, and foresee potential consolidation in the renewable energy advisory space.

- With Dallas nearby and sufficient land available, L-Z North in Texas is one of the hottest load zones in Texas for offsite renewables.

- We’ve got our eyes on the next iteration of the Los Angeles Department of Water and Power (LADWP) solar feed-in tariff program. Tune into the March edition of SOURCE for updates; we’re expecting an official announcement shortly.

- New Hampshire property owners are increasingly interested in solar, but policy constraints make it challenging for projects to pencil. Customers are only allowed retail net energy metering up to 100kW, and only projects up to 1MW may be interconnected. The New Hampshire Public Utilities Commission is currently exploring new alternative net metering tariffs and whether a cap on solar continues to be necessary.

- Legislation expanding Rhode Island’s Renewable Energy Growth program (RE Growth) has been filed in the House and Senate. Legislation would expand RE Growth for another 10-years at 40MW each year. Meanwhile, we’re watching closely for 2016’s first enrollment period to open.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered more than 500MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.