As the solar trade case loomed for much of last year, regulatory uncertainty drove price spikes. Now, three months after President Trump announced that he would be levying tariffs on solar modules and cells, the market is finally beginning to stabilize. Current module prices, which rest in the mid-to-upper 40’s (cents-per-watt) for standard models, may not be comfortable, but they now have a foundation free of the intense speculation that plagued much of 2017. Most importantly, as we look ahead at market dynamics and technology trends, we see a much clearer picture of future pricing.

Prices Now Can Start Falling Again

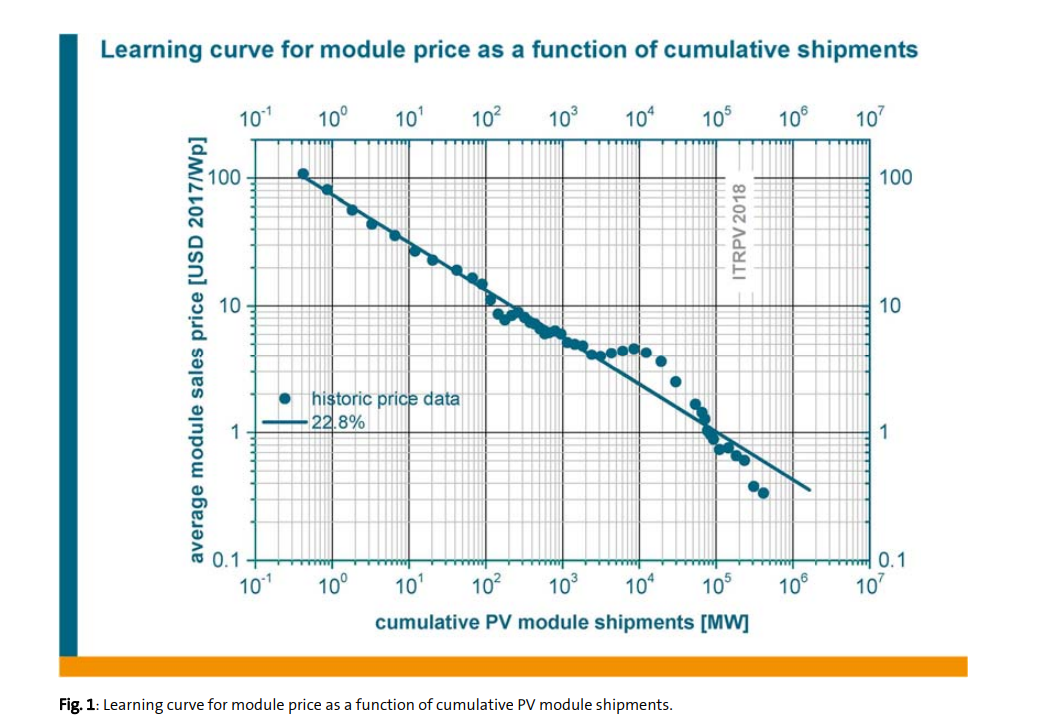

[caption id="attachment_5868" align="alignright" width="300"] Learning curve for module production. Source: ITRPV[/caption]

Learning curve for module production. Source: ITRPV[/caption]

Although prices have been raised by the tariffs, standard market behavior will continue to bring cost reductions to PV production, and in turn, prices. The International Technology Roadmap for Photovoltaic (ITRPV), which researches and reports trends in module technology and pricing, points to the steady learning curve in module production that has consistently caused price declines. With every doubling of cumulative module production, there has been a linear decrease in price to accompany it. In other words, as manufacturers continue to refine their products and processes, module efficiencies will be realized, and cost reductions will follow as a result. Based on Sol Systems’ analysis, we see the underlying tariff-free module prices falling back to their expected levels within a year. Put simply, now that the market has coalesced with more certainty around tariffs, tariff-included pricing can be predicted with more confidence, and price declines may occur yet again.

The PERCs of Higher-Efficiency

As industry-standard polycrystalline (poly) modules begin to decline towards pre-tariff pricing, new technologies are beginning to emerge in parallel. Higher-efficiency options, namely mono-PERC modules, are beginning to become more popular and widely-produced. Modules incorporating a mono-PERC treatment, which adds a reflective layer between the silicon wafer and the backsheet to send light back into the energy-producing part of the cell, look to have a bright future in the market.

The efficiency of these modules generates value for solar projects, even though their high-efficiency often leads to a price premium of 5-7 cents-per-watt. This is especially true for smaller commercial projects, specifically when they are space-constrained, as mono-PERC modules offer the perk (pun intended) of extra generation. By reducing the number of modules necessary to reach a system’s desired capacity, mono-PERC and other high-efficiency modules can help bring down balance-of-system (BOS) costs, namely by reducing the amount of labor necessary for installation of the system. For the carport market, which is hardest hit by the recent tariffs on steel, the addition of more capacity per unit of steel racking through high-efficiency modules like mono-PERC could lead to higher margins for developers. These variables are highly market-dependent, and developers will be making these decisions on a project-by-project basis.

As more mono-PERC modules are produced and put into service, we can expect to see price compression between mono-PERC and standard poly/monocrystalline modules. Given that mono-PERC is still a relatively new technology that is rapidly gaining scale in the global marketplace, price declines will be seen much faster than standard modules given the greater room to scale and improve. Our analysis shows that the current 25 percent premium developers pay for mono-PERC compared to poly modules is on track to shrink to just 10 percent by 2020. As this compression occurs, we can expect to see mono-PERC take increasingly more of the market share.

-

Even amidst tariffs, module price declines will continue to drive solar’s growth as a competitive energy source. True, module prices are sitting markedly higher now than a year ago, but the picture of a year from now is much clearer. As prices return to pre-tariff levels and lower in the coming years, that picture will continue to look better. Solar has plenty of momentum going into the future and as modules become less-expensive and more-efficient, that momentum will only build.

This is an excerpt from the April 2018 edition of The SOL SOURCE, a monthly electronic newsletter analyzing the latest trends in renewable energy based on our unique position in the solar industry. To receive future editions of the journal, please subscribe.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered 700MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.