It’s been an interesting few months for the solar industry. Uncertainty about the status and potential impact of tax rate reform, coupled with the gut-punch of the recent Suniva Section 201 filing, has made good news for investors and developers alike hard to come by.

However, behind the storm clouds, there is a potential silver lining for tax equity transactions… if tax reform is passed in 2018 or later. In fact, structured the right way, a tax rate decrease in 2018 could significantly boost the returns for a tax equity investor on any 2017 investment.

The key is the timing and allocation of the depreciation benefits. Assuming the solar Investment Tax Credit (ITC) is preserved, which we believe it will, a tax rate decrease is detrimental to the returns of a tax equity investor. This is because the value of the depreciation received from a solar investment is reduced in direct proportion to the reduction in corporate tax rates. For instance, if an investor were to receive $1mm in depreciation (losses) from a solar investment, at a marginal corporate tax rate of 35%, that depreciation offsets $350,000 of income tax liability elsewhere within the investor’s organization. If the tax rate is reduced to 20%, on the other hand, that same million dollars in depreciation is only worth $200,000 to the same investor. To protect against tax reform, a tax equity investor should seek to monetize as many losses as possible before rates drop – and then reap the rewards of a lower tax rate after their capital account is exhausted.

The portion of depreciation available to the investor will be limited by two factors: the structure determining the investor’s allocation of losses in 2017, and their ability to absorb those losses in 2017 (that is, their outside basis in the deal).

Structure

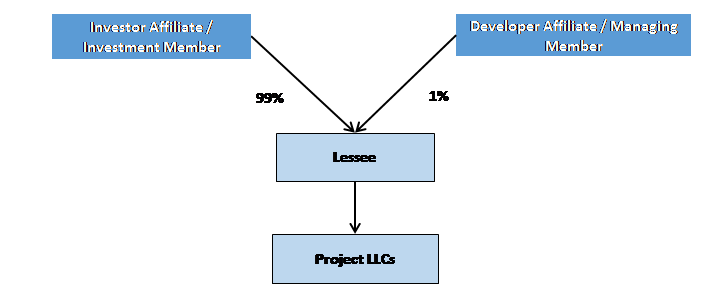

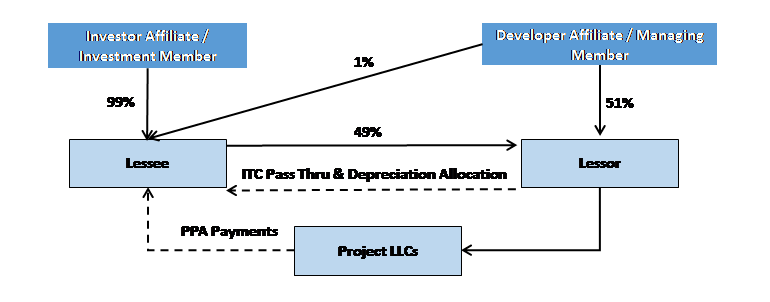

Investors using a partnership flip structure will be allocated 99% of taxable income or losses in Year 1. Electing bonus depreciation will almost certainly ensure they are allocated enough losses to turn a tax rate decrease from a problem into a benefit.

This issue is more complex for investors using the lease pass-through structure because they must allocate losses necessary to benefit from a tax rate decrease. We recommend these investors work with their tax counsel, accountants, and advisors (Sol Systems is happy to help) to follow guidelines on loss allocations and explore remedial allocation methodologies to allow for maximum loss allocation.

Basis

Allocating losses is only half the battle, however. The remaining challenge is to establish sufficient basis to monetize those losses in 2017. With most projects placing in service at the end of the year, an investor is often not called upon to make the bulk of its capital contributions until the following spring. If the investor has only paid in the minimum required portion of capital (20%) prior to commercial operations it cannot absorb the losses otherwise allocated to it. There are several options for overcoming this hurdle – one requires the smart application of minimum gain (where certain types of project-level debt can create additional basis for members), or a partial guarantee of construction debt, if present, to achieve the same effect. Barring the presence of any debt whatsoever, an interim contribution of capital at the end of the year will establish the requisite basis, and can be made after the projects have placed in service but prior to the end of the tax year.

Using either structure with the election of bonus depreciation, it is possible to monetize enough losses in 2017 such that the negative impact of a lower corporate tax rate on losses in future years is outweighed by the benefit of that lower rate on taxable income. The net effect can be a bump of several points on the investor’s return on investment.

Not every tax equity investor will have the appetite to examine the upside and downside inherent in each approach. However, for those willing to think through the risks and benefits of the coming changes, 2017 could be a “unicorn year” for yield-seeking investors.

This is an excerpt from the June 2017 edition of The SOL SOURCE, a monthly electronic newsletter analyzing the latest trends in renewable energy based on our unique position in the solar financing space. To view the full Journal, please subscribe or e-mail pr@solsystems.com.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered more than 600MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.