SOME (So Others Might Eat): Driving Impact through Meaningful Community Engagement

Insights |

By The Sol Systems Team

“Impact through Infrastructure” - While succinct, these words encapsulate Sol Systems’ commitment to driving positive societal impact. They are a call to action – a mission to empower and elevate the communities we serve as part of an equitable transition to a sustainable energy future. This effort is rooted in Sol Systems’ engagement with local leaders and partners to foster an approach to sustainable infrastructure that pairs solar energy projects with long-term investments in ecosystems and communities disproportionately impacted by climate change.

In this edition of our Infrastructure + Impact Spotlight Series, we pay homage to our partner, SOME, an interfaith community-based service organization whose mission is to break the cycle of poverty and homelessness through programs and services that help transform lives of individuals and families, their communities, and the systems and structures that affect them. Each day, SOME strives to restore hope and dignity one person at a time through its integrated “Whole Person Care” approach. What began as a lunch line on the corner of North Capitol and K Street more than 50 years ago has flourished into an esteemed leader for affordable housing, healthcare, rehabilitative services, education, employment training, and food security throughout Washington, D.C.

SOME is actively redefining affordable housing in the District by creating a stable foundation where its residents can explore their potential. SOME provides transitional housing programs for those earning 30% or less of the Family Median Income ($38,700 for a family of four as of 2021) while ensuring that residents progress by teaching them to create budgets, financial goals, and sustainable payment plans. Since opening its first transitional housing program in 1986, SOME now operates a portfolio of over 1,300 affordable housing units for single adults, families, and senior citizens, preparing them for homeownership or market-rate rents through a step-by-step process.

Take the Bonner Family, for example. Their time living in SOME's two-year accelerated housing program helped them make great strides. During the pandemic, with the program's help, the Bonners saved over $14,000 in housing costs and more than $800 in emergency savings, all while paying off their credit card debt and building a strong credit score, allowing them to move into a new home in the District in 2022.

Photo credit: The Bonner Family

This dynamic approach to care is especially critical in a city like Washington, D.C., where in the past two decades, the number of affordable housing units has decreased while the number of high-cost housing units has multiplied. [1] The resulting structural barriers continue to affect low-income residents’ ability to afford safe and healthy housing, food, and utilities, among other necessities.

It is because of these realities that Sol Systems remains committed to supporting community leaders like SOME to fill critical gaps by leveraging the benefits of sustainable infrastructure such as solar energy, energy efficiency and critical home health and safety upgrades to drive positive environmental and community impacts beyond the carbon reduction inherent in clean energy. In the spirit of this partnership, on May 17th, 2022, Sol Systems, FedEx, and SOME announced a special arrangement that spreads the benefits of the Sol Systems-developed 915 kW rooftop community solar project at the FedEx Express Eckington Place facility even further into the District. FedEx is allocating the bill credits generated from the solar installation, along with a supplemental cash donation, to SOME to offset the annual electricity costs at two of its facilities located in Ward 5 – Weinberg House, an affordable housing facility that is home to 28 families and Isaiah House, home to a day program for homeless adults with severe and persistent mental illness. Beyond this immediate impact, reducing the energy burden of these facilities will enhance SOME’s ability to devote additional resources to initiatives that empower its clients to create long-term, sustainable change.

Sol Systems’ commitment to under-resourced communities is a priority shared by the leadership and staff. On April 20th, 2022, we joined SOME to celebrate Earth Day by working on beautification projects at Zagami House – one of SOME’s housing sites where Sol Systems had previously made contributions toward HVAC and energy efficient appliance upgrades. The projects, which included planting of seasonal flowers, assembly of raised garden beds, and mulching of playground areas revitalized Zagami’s grounds for residents to enjoy. Partnering with organizations like SOME shows how meaningful collaboration with communities can help to tackle local challenges and ensure that all communities participate in the clean energy economy. To learn more about how SOME drives impact through meaningful community engagement, please visit SOME’s website at: SOME.org.

Exploring Agrivoltaics: Solar Design and Lettuce Yield in Fresno, California

Insights |

By The Sol Systems Team

This article is part of the March 2023 edition of our publication The Sol SOURCE. Click here to read the full publication.

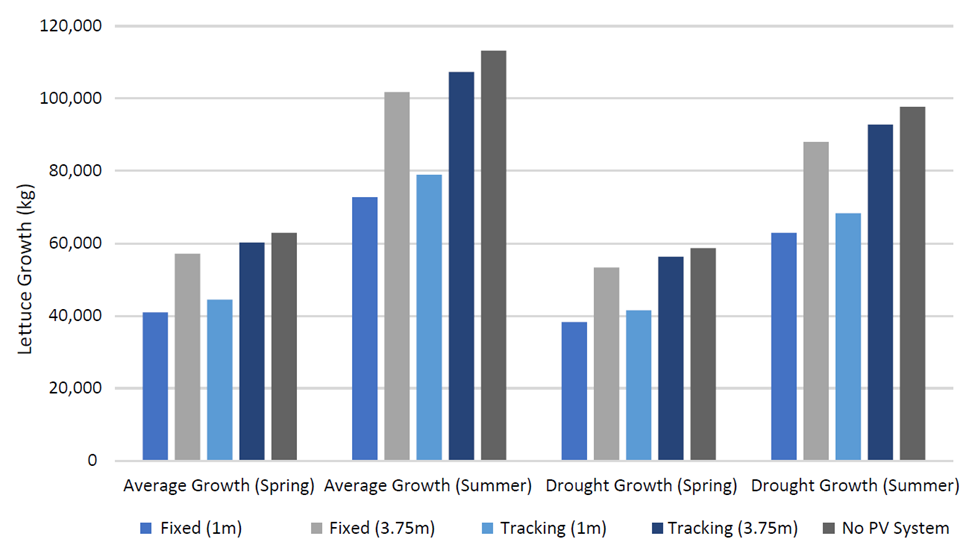

The agricultural and solar industries sometimes compete for land use, but they have recently found ways to work together. Agrivoltaics is the use of land below solar panels for crop fields, allowing a site to produce both food and energy. To better understand how these dual uses interact, we researched how yields for lettuce, a cash crop that can produce in shaded conditions, might benefit from changes to solar panel configuration at a projected growing site near Fresno, California. We found that some configurations are well suited to both agricultural productivity and project returns.

Research Methods

Our team evaluated four system configurations:

a fixed ground-mounted system with one-meter ground clearance;

a fixed elevated system with 3.75-meter ground clearance;

a single-axis tracking ground-mounted system with one-meter ground clearance; and

a single-axis tracking elevated system with 3.75-meter ground clearance.

We measured the effect on lettuce yield of adjustments to ground-clearance height, array height, axis selection, tilt, tracking rotation limit, and backtracking.

Row spacing was set to approximately four meters between panels, allowing lettuce positioning between rows to conform to standard 14-inch spacing, including 14 inches from the system’s standard 20-inch-diameter support piling. The yield was measured under normal and drought conditions to monitor crop response to variable moisture retention. Reduced moisture retention in drought conditions results in greater production when panels are positioned over the lettuce, enhancing yield for ground-mounted panels and elevated arrays.

Using all input parameters, we created 25 plots of subarrays containing 20 rows per subarray and 16 modules per row, occupying a total of seven acres of land. Differences in assumed yield were calculated based on average photosynthesis. System costs were adjusted to reflect increased labor and materials costs of elevating panels on stilts and installing trackers.

Results and Conclusion

Total lettuce output for each system parameter demonstrated that elevating panels is key to increasing lettuce yield. Tracking also increases yield, although to a lesser extent.

The cost-adjusted financial results for each array design showed that the fixed elevated system generated the highest net present value, while the ground-mounted tracking system generated the highest internal rate of return (IRR).The elevated tracking system maximized lettuce yield, generated the highest total income, and generated a greater IRR than both fixed systems. The single-axis tracking array with 3.75-meter ground clearance resulted in the smallest reduction in lettuce yield compared to full-irradiance growing conditions. Importantly, an elevated system design would allow tractors averaging three meters in height to pass under the array, allowing farmers to use typical harvesting techniques. Unelevated ground-mounted systems would require harvesting by hand, necessitating special protective equipment for workers operating near the panels.

Further research into the potential of agrivoltaics is essential to improving land use in the clean-energy economy. More detailed data and citation information are available upon request.

Endnotes

1. Barron-Gafford, Pavao-Zuckerman, Minor, Sutter, Barnett-Moreno, Blackett, Thompson, Dimond, Gerlak, Nabhan, and Macknick (2019), Agrivoltatics provide mutual benefits across the food-energy-water nexus in drylands, Nature Sustainability.

2. Tani, Suguru, Nakashima, and Hayashi (2014), Improvement in lettuce growth by light diffusion under solar panels, Journal of Agricultural Meteorology.

Solar importers need clearer guidelines from U.S. Customs and Border Protection (CBP) under the Uyghur Forced Labor Prevention Act (UFLPA). The UFLPA is the latest in a series of trade interventions with crucial implications for the deployment of solar technologies to take effect in the last year.

Specifically, the UFLPA prohibits imports into the United States of any goods mined or produced using forced labor from the Xinjiang Uyghur Autonomous Region of China. CBP began enforcing the law on June 21, 2022. While the UFLPA targets a broad range of imports, solar panels have been a focus. CBP issued further guidance on June 13, 2022, citing manufacture of polysilicon—a critical component in solar panels—among the sectors with the highest risk of exposure to forced labor in Xinjiang. As of August, enforcement of the UFLPA has already resulted in more than three gigawatts’ worth of module detentions by CBP. Given its influence on the global photovoltaic supply chain, and especially in light of concurrent federal investments made to scale up domestic solar manufacturing, the Act’s enforcement remains critical.

The UFLPA’s reinforcement of existing U.S. regulations against forced labor comes in response to the state-sponsored detainment of more than 1.8 million Uyghurs and other Muslim minority groups in a system of mass internment camps in Xinjiang, China. Having recently navigated a CBP-issued Withhold Release Order (WRO) of a similar nature, solar module suppliers and their consumers are committed to identifying and removing forced labor from their supply chains. The UFLPA, however, heightens the evidentiary standard imposed on U.S. importers by rebuttably presuming that all goods mined, produced, or manufactured “wholly or in part” in Xinjiang or by entities listed on the Department of Homeland Security’s entity list are made using forced labor. Such goods are therefore denied entry into the U.S. unless an importer can “clearly and convincingly” prove that its imports are (i) outside the scope of the UFLPA, so that the presumption does not apply, or (ii) within scope but eligible for an exception. Rebutting the Act’s presumption requires substantive supply-chain documentation that ties every component in a product to a source that is free of forced labor. To that end, importers have so far relied on affidavits from suppliers attesting to the origin of their products while also collecting bills of lading, production records, invoices, and other supporting evidence. CBP should streamline the process for importers providing such information and increase the number of solar panels and critical components that are allowed to pass across U.S. borders.

Raw materials from Xinjiang are found in dozens of supply chains across the agriculture, healthcare, manufacturing, and energy industries; but because nearly half of the global supply of polysilicon comes from Xinjiang, CBP’s enforcement of the Act means that U.S. solar developers will continue to struggle until CBP provides transparent guidance on import requirements and documentation. Similarly to the Department of Commerce’s ongoing circumvention investigation, whose mere initiation put 51 GW of solar capacity and $52 billion of utility-scale investment at risk, the UFLPA is set to prevent as much as 12 GW of solar modules from entering U.S. markets by the end of 2022. According to AnnMarie Highsmith, Chief of Trade for CBP, as of September the agency had yet to receive any applications from importers for what it calls admissibility reviews, or requests to rebut the Act’s presumption using documentation. Instead, Customs has processed several requests for applicability reviews—claims by importers that goods currently detained by CBP have no connection to Xinjiang or restricted entities.

The American solar industry is taking the fight against human-rights abuses seriously. Many companies have reoriented their supply chains and onboarded third-party audit procedures to avoid using polysilicon sourced from anywhere in the Xinjiang region, and with the support of the Biden Administration, the Solar Energy Industries Association (SEIA) has taken steps to turn an internal supply-chain traceability protocol into an industry standard. However, it is essential for CBP to provide clearer guidance and systematic procedures for solar imports.

Inflation Reduction Act Charts New Path for Clean Energy

Policy |

By The Sol Systems Team

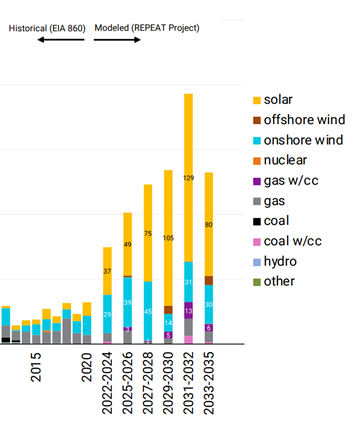

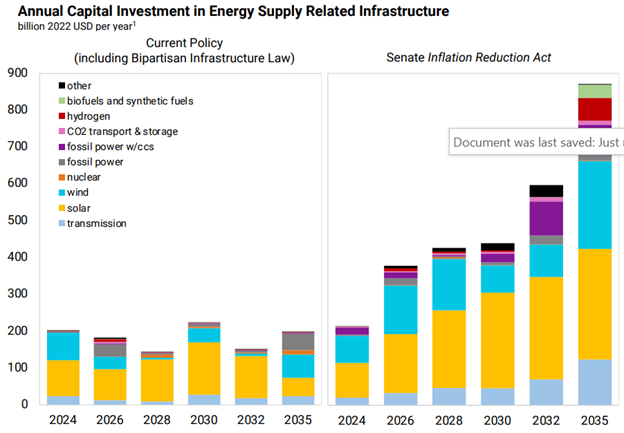

A new generation of clean energy begins in the United States. As the Inflation Reduction Act of 2022 (IRA) becomes law, we embark on new and historic opportunities for developers, investors, and renewable energy buyers. Numerous analyses demonstrate the clean energy and climate provisions of the IRA will spur economy-wide greenhouse gas emission reductions of 40 percent while beginning to reshore critical manufacturing supply chains. This will allow corporate leaders to accelerate clean energy investments and to make more impactful energy procurement decisions as the IRA begins the process of addressing historical energy inequities in communities across America.

Additionally, the IRA will spur new technological growth which will lead to new clean energy resources and increased project availability for energy buyers across the US. Energy Innovation also found that the IRA could create up to 1.5 million jobs by 2030. Underpinning the success of the IRA is the need to scale the renewable energy sector. Wood Mackenzie estimates that, at a minimum, the IRA will lead to 67% more solar.

Figure 1. Historical capacity additions and protections under the Act (GW)

What’s in a Name?

In our last CEO letter, we highlighted the threat that inflation poses to the renewable energy industry while noting the deflationary potential of clean energy. The aptly named Inflation Reduction Act’s monumental investments in clean energy should have a long-term deflationary impact.

What’s in the Law?

Clean Energy Tax Credits

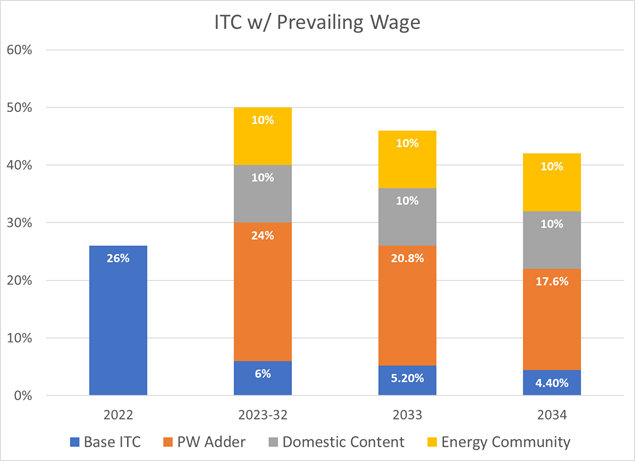

Among other credits, the clean energy tax credits in the IRA maintain the historic standalone solar ITC until 2025 when the credit shifts to technology-neutral. Essentially, after 2025 the IRA tax credits incentivize any method of generating electricity without emitting carbon dioxide (CO2). This includes stand-alone energy storage, clean hydrogen, and advanced and existing nuclear, as well as domestic manufacturing. Additionally, credit recipients, including solar, now have the option to select either the investment tax credit (ITC) or production tax credit (PTC). We anticipate that most solar operators will continue to prefer the ITC, at least in the initial years. The below illustrates the base ITC and adders available to larger solar projects meeting labor requirements (additional incentives are available for smaller projects, including the ability to consider interconnection costs in calculating total project cost eligible for the ITC). These credits will begin to phase out the later of 2032 or when the electric power sector emits 75 percent less CO2 than 2022 levels. This will for the first time directly connect clean energy credits to decarbonization goal, and ensure they are available to achieve it.

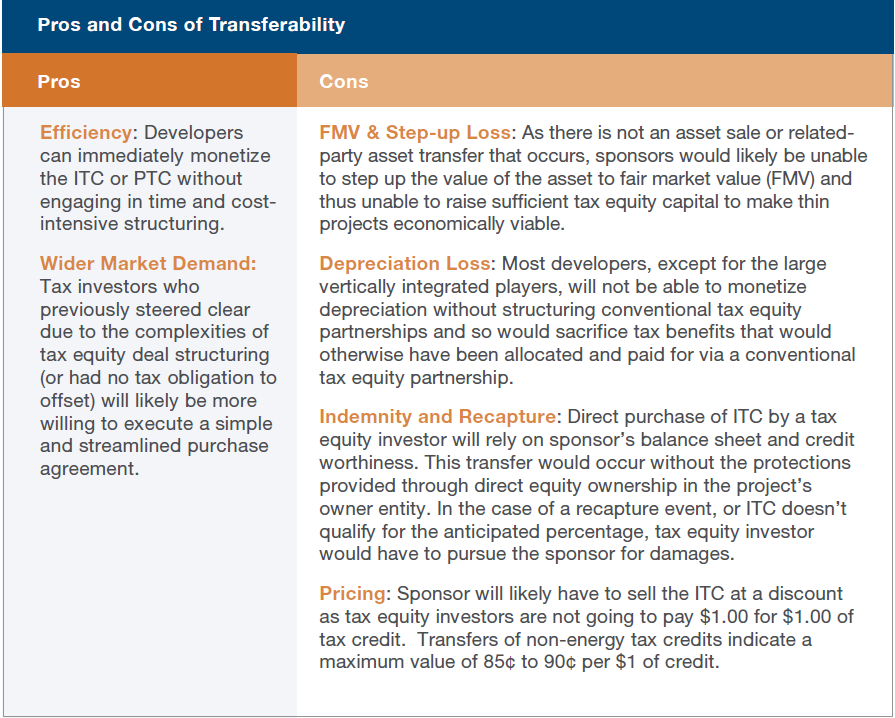

Important to note that the IRA sets the base ITC at siAlthough we expect that the IRA’s new direct-pay and transferability options will allow new participants without tax obligations, such as electric cooperatives and municipal utilities, to construct renewables, we do not expect the new options to slow appetite for traditional structured tax equity transactions. To begin with, we expect guidance and initial demonstration of the new options to take at least a year, advantaging traditional tax equity investments in the near term. But even over the longer term, we expect structured tax equity financing will remain more attractive to corporate partners because of its lower recapture risk, its ability to monetize depreciation, and the opportunity it provides for projects to be valued at fair market value rather than cost. The chart below provides a high-level overview of the advantages and disadvantages of transferability versus structuring from a sponsor’s perspective.

Beyond the changes in methodology for investors to acquire tax credits, the IRA allows solar projects to elect Production Tax Credits (PTC) instead. This opens the possibility of structuring a PTC investment similar to the PAYGO financing tax equity structure that exists in the wind segment of the market today. Within the solar space, this could provide additional benefit in geographies with high yields and where production is highly predictable.

Implications for Developers

We expect a limited positive impact on current projects given that the 2022 ITC rate has now increased to 30 percent from the expected 26 percent without triggering labor requirements. We expect this 30 percent to extend into 2023 and for 60 days after the IRS issues new guidance, giving near-term projects an unexpected boost. In addition, the new adders available for projects in fossil fuel transition communities “energy communities” and for projects incorporating domestic content will drive needed investment in both. The

Broad Tax Changes that

IRA seeks to drive clean investment in “energy communities, which may be thought of as energy transition communities – communities that have borne the brunt of fossil fuel usage and should not be left behind in the shift to clean energy. Per the IRA, energy communities include:

Brownfield sites,

Areas with high historical fossil fuel employment and currently high unemployment, and

Areas where coal mines and/or coal-fired power plants have closed.

Thus, a strong financial incentive for projects in energy communities will allow them to continue powering America, but with new access to clean energy resources and funding. In addition to the clean energy and climate benefits, the IRA’s investment in energy communities will have untold public health benefits for communities that have been disproportionately impacted for too long.

Clean Energy Tax Credits

Among other credits, the clean energy tax credits in the IRA maintain the historic standalone solar ITC until 2025 when the credit shifts to technology-neutral. Essentially, after 2025 the IRA tax credits incentivize any method of generating electricity without emitting carbon dioxide (CO2). This includes stand-alone energy storage, clean hydrogen, and advanced and existing nuclear, as well as domestic manufacturing. Additionally, credit recipients, including solar, now have the option to select either the investment tax credit (ITC) or production tax credit (PTC). We anticipate that most solar operators will continue to prefer the ITC, at least in the initial years. The below illustrates the base ITC and adders available to larger solar projects meeting labor requirements (additional incentives are available for smaller projects, including the ability to consider interconnection costs in calculating total project cost eligible for the ITC). These credits will begin to phase out the later of 2032 or when the electric power sector emits 75 percent less CO2 than 2022 levels. This will for the first time directly connect clean energy credits to decarbonization goal, and ensure they are available to achieve it.

Important to note that the IRA sets the base ITC at six percent if new labor conditions are not met, but allows for a step-up to 30 percent if labor conditions are met (the PTC is similarly structured). In order to receive the full ITC (or PTC), prevailing-wage labor requirements must be met for all projects over one megawatt (MW). This includes:

Payment of prevailing wages during construction, as well as for labor on repairs or alterations during the five-year recapture period on the ITC (for projects over one MW).

Use of sufficient apprenticeship ratios, unless demonstrably unavailable.

Additive ITC bonuses would be available for sufficient use of domestic content as well as construction in an energy community. At 10 percent each, a 50 percent ITC is possible for projects that meet both additional criteria. For smaller projects, an additional 10–20 percent is available for solar projects located in certain low-income communities, low-income residential buildings, or on tribal land.

Transmission upgrades would be considered qualifying property for the calculation of the ITC when part of a project under five MW.

Additionally, for the first time the IRA extends “direct pay” of tax credits to non-profit entities for all resource types and for a limited time to all entities for new categories, such as carbon capture and storage (CCS). Direct pay means that qualifying entities may elect to receive a direct payment of the value of the credit, eliminating the need for participation by an investor with a sufficient tax obligation to monetize them. Entities not eligible for direct pay, including for-profit businesses, are allowed a one-time transfer of each year’s eligible credits to an unrelated taxpayer. We will continue to assess the pros and cons of the new transferability provisions as compared to traditional tax equity financing. Transferability will be effective in early 2023, although forthcoming IRS guidance is necessary to answer questions about how it will work.

Broad Tax Changes that Affect Solar Financing

Several general tax provisions have implications for clean energy financing, most notably the new rules regarding calculation of corporate taxes. For taxable years beginning after 2022, the IRA will apply an alternative minimum tax to C-corporations that have an average annual adjusted financial statement income (i.e., “book” income) for any three-year period in excess of $1 billion. The IRA does not change existing depreciation schedules, but bonus depreciation benefits are slated to phase out between 2023 and 2026, which may have longer term impacts on project finance, as discussed further below.

What’s Next?

What is clearer now than ever before is that clean energy will drive domestic climate action and provide new opportunities for renewable energy growth, procurement, and investment. President Biden signed the IRA on August 16, 2022, and now it heads to the Internal Revenue Service (IRS) for implementation and guidance. While the IRA provides a domestic path to begin building a better tomorrow, it is now on the shoulders of the renewable energy community to execute on the tasks ahead of us and to ensure the future we create is one that benefits all.

Assessing Current and Emerging Technologies in Solar Energy

Technology |

By The Sol Systems Team

New technology and scale continue to drive advancements in renewable energy. This is an exciting time for solar technology, particularly as implementation of the Inflation Reduction Act (IRA) begins. Here, we highlight some of the market and current and some future technological trends in solar energy.

High Material Cost is Causing Strategy Adjustments for Developers

In June of 2020, previously record-low spot market prices for polysilicon began to rise, a trend we expect to continue into 2023. With it, the cost to build solar energy began to increase for the first time in a decade, and unexpectedly high procurement costs have left developers looking to reduce supply-chain and logistics cost, in part, by maximizing system capacity and size. As a result, the physical size of solar modules, along with the inverters, cables, and transformers necessary to facilitate them is increasing. Before we delve into the details, it’s important to understand the basic facts underlying new module technologies.

Mono-PERC Dominant as Bifacial Market Share Increases

In 2018, we wrote about how premium, higher-efficiency cell technologies, like monocrystalline PERC (mono-PERC) modules, were beginning to close the price gap with non-premium modules. The price gap is now non-existent, and mono-PERC cells dominated the market with a market share of 85 percent in 2021 (and likely much higher when considering only the U.S. market). Mono-PERC cells have impressive energy conversion efficiency that currently averages approximately 21 percent, and their consolidated market share has helped reduce cost at scale. In addition, roughly half of 2021 solar installations incorporated the use of bifacial modules, which only further increases efficiency of projects. Before 2020, bifacial modules only made-up approximately 15 percent of the overall module market, but is now expected to exceed 85 percent by 2032 (this should continue or even increase with continued exemption of bifacial modules from Section 201 tariffs). In brief, today’s utility-scale solar projects are now overwhelmingly using bifacial mono-PERC cell technology, considered a premium just a few years ago.

Decreasing Levelized Cost of Energy (LCOE) in the Face of Rising Build Costs

Increased module sizing has been key to bringing down the levelized cost of energy (LCOE) for solar, particularly in the utility-scale sector. In the second quarter of 2022, modules with 182 to 210 millimeters (mm) sized cells accounted for 80 percent of module shipments. The increase is notable when compared to 2018, when the previous standard 156.75 mm cells dominated the market with an approximate 90 percent market share. Developers that were installing 400 to 450 watt (W) modules in recent years are now routinely installing 600W or larger modules, and the modules with 210 mm cells alone are expected to reach 56 percent market share by 2023.

The implementation of larger-format modules results in changes to the equipment, cost, and overall layout of a site. The use of larger modules typically results in the need to upscale other equipment, such as racking systems. This can lead to an overall reduction in LCOE of the project, as developers are able build larger capacity systems using larger components that require less labor, transportation, and operations and maintenance (O&M) costs. As module sizes increase, however, installation will eventually become more difficult and single-axis trackers will require thicker foundations and torque tubes to maintain structural stability under increased wind loading. Thus, over the longer term we expect a plateau to size increase and a continued focus on efficiency improvements. In the meantime, larger-format modules are helping utility-scale projects pencil in the wake of an unusually expensive market.

What does Tomorrow’s Solar Look Like?

While we can expect the continued adoption of larger format bifacial modules in the near term, emerging technologies continue to seek market share in the coming years. Two versatile technologies peak our interest: perovskite-based solar cells and luminescent solar concentrators.

Perovskite solar cells are an emerging thin-film cell technology built using the calcium titanic oxide mineral perovskite rather than silicon. Following years of fast improvement, researchers recently achieved efficiencies greater than 30 percent in lab environments by combining perovskite with silicon in what are called tandem cells. This flexible, lightweight, and high-efficiency technology offers appealing potential in a variety of applications ranging from buildings to vehicles. While lab results are promising, the technology faces many barriers to commercial viability. Perovskite-based cells have long suffered a high rate of degradation, and solving the technology’s durability issues will be key to its prospects of competing with current technologies that continue to extend project lifetimes. While the technology has the potential to be relatively low cost, it has yet to pave a clear path to a commercially viable product that can be manufactured at scale.

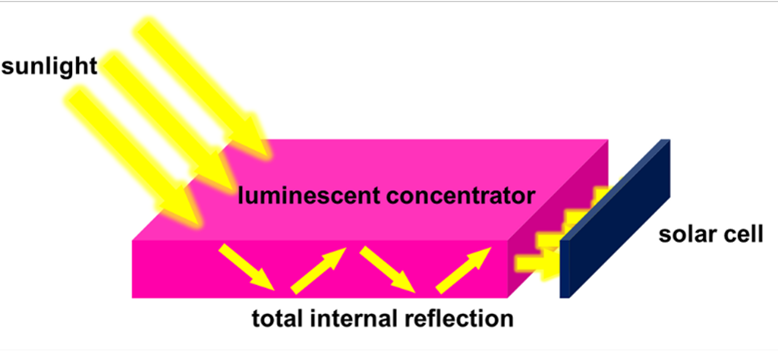

While perovskite technology is an example of a new, highly efficient solar cell that is achieving impressive results in ideal lab conditions, technologies like luminescent solar concentrators (LCSs), which use existing cell technology present an interesting near-term opportunity. In a lab testing environment, LCSs achieves ideal results by concentrating the highest magnitude of irradiance directly perpendicular to the cell. In other words, direct sunlight which is far from field conditions. LSCs, however, can efficiently convert irradiance in the field regardless of magnitude or angle of incidence through solar concentration.

A diagram illustrating how luminescent solar concentrators work – Credit: 4TU

LSCs look like a translucent, usually colorful, piece of plastic that glows slightly around the edges. Whereas solar modules absorb light directly into the cell at the angle the sunlight hits it, LSCs absorb incoming radiation into the material, trapping it there through a phenomenon known as total internal reflection. This trapped irradiance (concentration) is then concentrated directly in solar cells at the edge of the material, giving it the ability to harness diffuse irradiance similar to lab conditions.

A quantum dot LSC window - Credit: NREL

Because of its ability to efficiently convert diffuse irradiance into electricity, as well as its largely transparent material, LSCs are becoming a more practical and less expensive way to integrate solar cells into applications like windows. This could allow solar generation using a building’s façade rather than just its roof. Additionally, recent breakthroughs in “quantum dot solar concentrators,” provide a longer life and a wider variety of colors for LSCs, which could lead to a clearer path for future commercial viability.

-

Scaling the solar industry at a rate necessary to succeed under the Inflation Reduction Act (IRA) will require increasingly innovative solar design and deployment. We look forward to keeping you updated as technology continues to evolve.

GETting from Here to There: Grid-Enhancing Technologies Mature

Technology |

By The Sol Systems Team

One notable challenge of the American energy transition lies in modernizing the transmission grid at a pace that reliably integrates the enormous growth of clean and renewable energy. With federal clean energy investments like the recently-signed Inflation Reduction Act (IRA) incentivizing the development of wind and solar power projects faster than the grid can expand, new grid-enhancing technologies (GETs) can offer a bridge between the speed of generation built and the ability of the grid to catch up. Simply put, in the decade that it takes to build new transmission lines, GETs can be deployed in a matter of months and alleviate grid congestion keeping renewables in the queue. One such technology, dynamic line ratings (DLRs), has the potential to ease congestion on transmission lines and enhance safety and reliability by improving the accuracy and transparency of line ratings. Not only would these improvements provide much-needed consumer savings, but they would reduce the cost and increase the speed of interconnecting more solar and wind power resources as well.

For decades, many North American transmission operators have used static line ratings (SLRs) to determine the maximum power flow capacity on a transmission line. Appropriate for the mid-20th century grid, SLR calculations use intrinsically conservative assumptions regarding atmospheric operating conditions to produce transmission constraints that vastly underestimate how much power lines can carry. Using modern computing power and digital monitoring, DLR systems, by contrast, paint a more accurate picture of transmission line capacity by accounting for the role of real-world conditions such as rain, air temperature, cloud cover, and wind speed. This ambient approach to grid management can both reveal significantly greater transmission capacity than previously presumed while also detecting situations where flows should be reduced for safe and reliable operation.

As the demand for clean electricity continues to grow, misaligned regulatory and economic incentives have caused transmission gridlocks with multibillion-dollar congestion costs while also preventing the interconnection of over 70 percent of the new renewables and nuclear capacity needed to hit climate targets set by the Biden Administration and a growing number of states. On February 17, 2022, the Federal Energy Regulatory Commission (FERC) launched an inquiry aimed at evaluating the benefits, costs, and challenges of DLR implementation. Furthermore, several utilities like New England’s National Grid and New York’s Power Authority have begun piloting DLR systems on transmission lines across their service territories. The recently passed Inflation Reduction Act, with its long-term solar and storage tax incentives, serves as further evidence of the tide turning toward a future beyond wires that includes a broader range of transmission technologies. No one is touting GETs as the panacea to the climate crisis nor is their optimal deployment as simple as dropping DLR systems on every transmission line. Not up for debate, however, is that grid capacity must expand in coming years to integrate an ever-evolving resource mix efficiently and reliably. To that end, grid-enhancing technologies present a viable alternative capable of spurring the cost-effective transmission infrastructure that will help decarbonize the electric grid with significant clean energy deployment.

{kind=link}