The Sol SOURCE is a monthly journal that our team distributes to our network of clients and solar stakeholders. Our newsletter contains energy statistics from current real-life renewables projects, trends, and observations gained through monthly interviews with our team, and it incorporates news from a variety of industry resources.

Below, we have included excerpts from the November 2017 edition. To receive future Journals, please subscribe or email pr@solsystems.com.

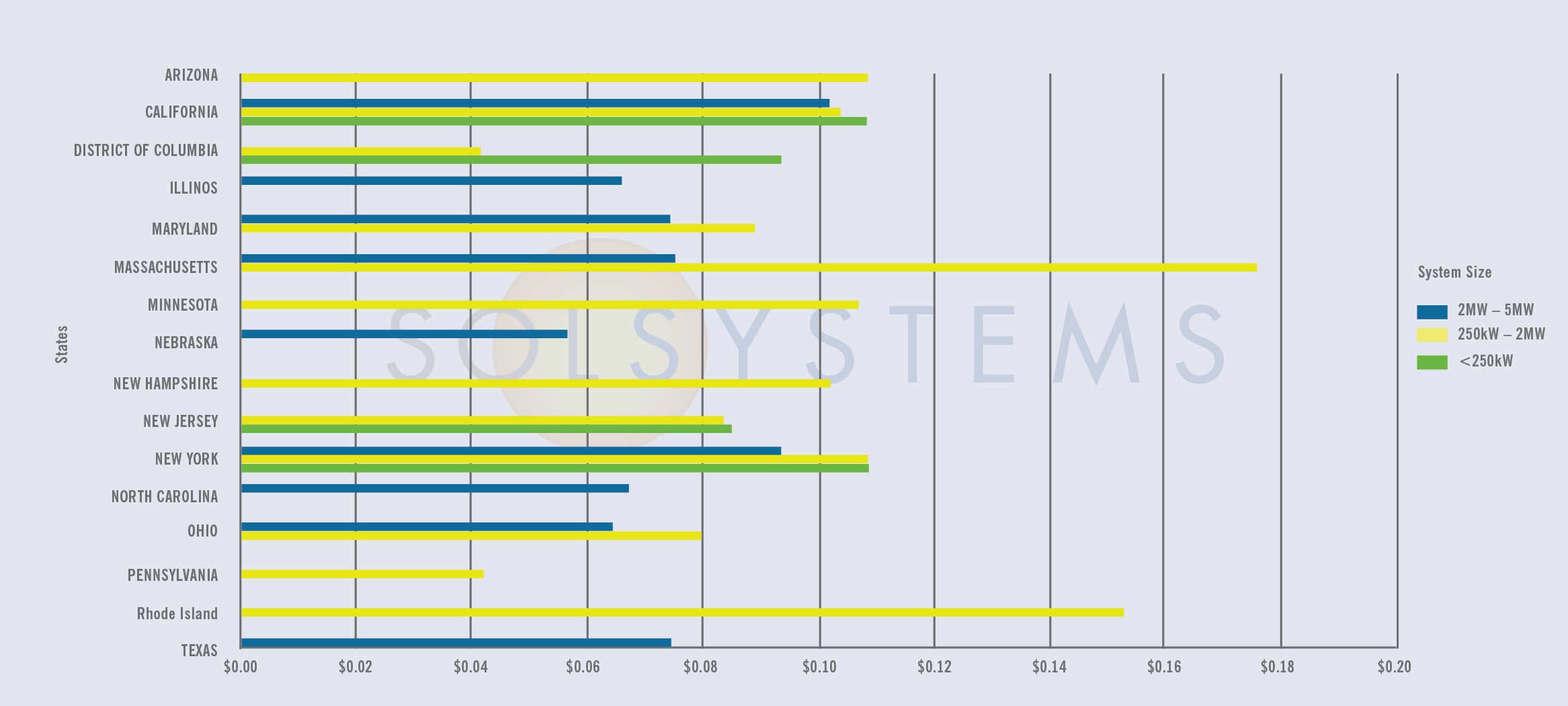

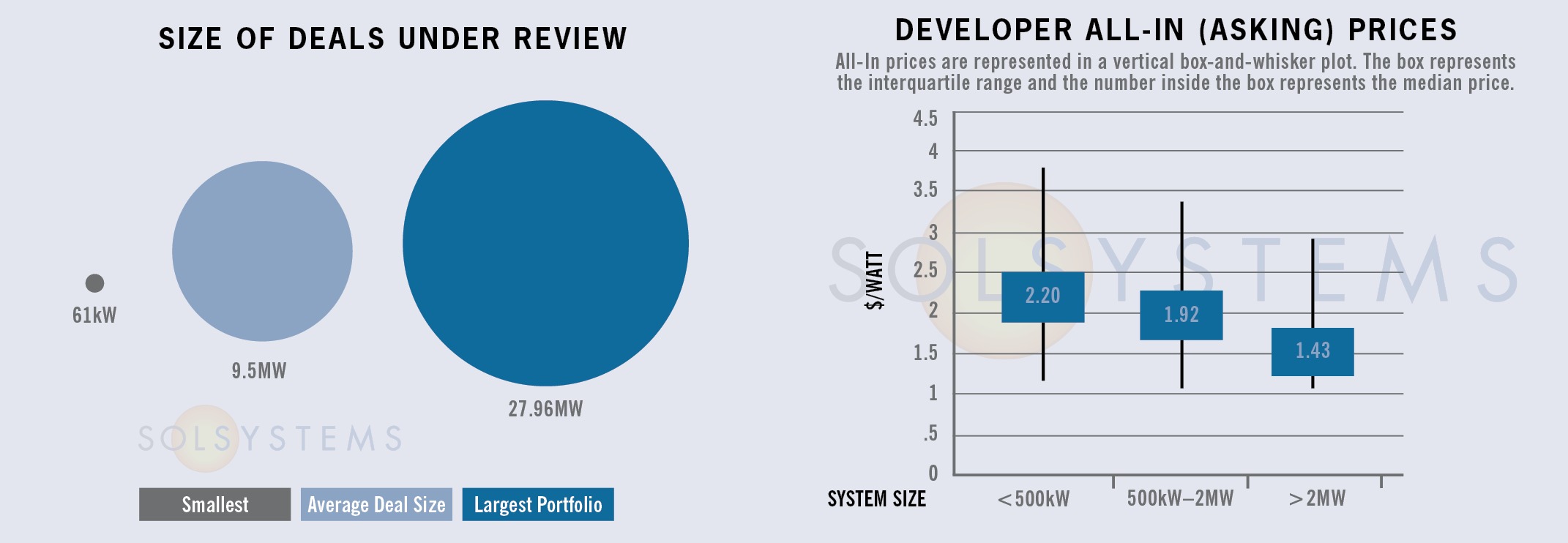

PROJECT FINANCE STATISTICS

The following statistics represent some high-quality solar projects and portfolios that we are actively reviewing for investment.

STATE MARKETS

New Jersey – As expected, Democratic gubernatorial candidate Phil Murphy won the Governor’s race in New Jersey this month. The vote was no surprise given his predecessor’s how-low-can-you-go approval ratings, but what will an administration change mean for the solar industry? Efforts to “pull forward” New Jersey’s solar carve-out from 4.1% by 2028 to 4.1% by 2021 were stalled last year, largely due to uncertainty that Governor Christie would sign the legislation. Since then, even more aggressive RPS legislation has been substituted for the pull forward, proposing an ambitious 5.3% solar carve-out by energy year 2021 ] Given that Phil Murphy will become Governor early next year, the odds for a more ambitious RPS package and net metering cap lift are all the more likely [if not early next year, then after an Energy Master Plan is crafted]. Murphy campaigned on a 100% RPS, something that would benefit all renewables, and not just solar.

New York – There is a growing sentiment that New York not only needs to, but will, revise its commercial and industrial (C&I) Megawatt Block program for rooftop solar. There are no details to be had yet, but one thing that is important is that people with a project reservation that will not go forward should facilitate the market by pulling their reservation out of the queue. This will help program administrators to realistically gauge the success of the program, and also better understand the budget available to provide a fix. Meanwhile, the value of distributed energy resources (VDER) continues to confuse not only developers, but proves increasingly challenging to message to customers.

Pennsylvania – It’s official. After years of advocacy from Pennsylvania SEIA and its allies, Pennsylvania has officially closed its borders to out of state solar renewable energy credits (SRECs). What does that mean?

As context, Pennsylvania was the only remaining SREC state that allowed generators from anywhere in the PJM region to sell into its market. As a result, solar projects built in PJM in utility-scale markets such as Virginia or North Carolina, or even rooftop homeowners in Ohio, could sell every 1000 kilowatt hours – which is one SREC–into the state’s solar carve-out program as allowed previously by PA’s Alternative Energy Portfolio Standard (AEPS). This abundance of RECs meant that complying with the state’s very modest .5% by 2021 (yes, one half of one percent, as compared to the 5.3% being discussed in New Jersey) solar carve-out has been easy, and the market has been perpetually oversupplied. As of November 1, RECs in Pennsylvania were valued at $4/SREC. Low SREC prices have led to very little in-state build; SEIA estimates that only 38.8MW of solar were installed in 2016. For comparison, SRECs in neighboring New Jersey are valued at $196/REC, and last year, New Jersey installed nearly ten times the solar as PA at a whopping 361.4MW. New Jersey is also home to over 6,000 solar jobs, while PA employs only half that amount.

Does this mean that the solar market will rebound? Not necessarily, largely due to the already abundant oversupply combined with a modest renewables target. The legislation also grandfathers certifications (as it should to avoid lawsuits) granted by the effective date of the law, October 30th, as well as solar generators already under contract. The latter language is especially murky, and as compliance entities typically contract under a REC volume, not an individual system, which may create challenges with enforcement. As a result, the law’s actual effects are to be determined, and the contracts language in particular will be subject to Public Utilities Commission interpretation.

In sum, the PA closed borders bill is a great, first step, and even more importantly, it shows that solar has bipartisan support in the PA legislature. With other states looking at 25%, 40%, or even 50% renewable energy targets, an AEPS increase in the coming years would be even better for stimulating development in PA – and seems possible after solar gained new allies with this bill.

SOLAR CHATTER

- Community solar in Illinois is this season’s “it” market, and at Solar Power Midwest, it was clear that developers with pipeline in New York, Minnesota, and even Massachusetts are now shifting their focus to Illinois. Need a refresher on the Land of Lincoln’s emerging solar market? We’ve got you covered.

- Updates to Michigan’s PURPA rules, something that we have been following for quite some time, could become a reality by as soon of the end of this month (pending Michigan Public Service Commission final orders). By updating its avoided cost methodology, creating 20-year contract terms, and standardizing avoided cost rates for small qualifying facilities (QFs) sized under 2MW, Michigan could become a new hot market for small utility-scale development. For more information, check out this summary from our friends at the Environmental Law & Policy Center.

- With the Suniva trade case looming, it has been an interesting year on the solar coaster for many in this industry. In our opinion, operations and maintenance (O&M) companies are some of the most resilient in the solar industry right now due to the recurring nature of their revenue streams and a quickly growing market for their services.

- We were expecting the initial procurement for SMART, the new Massachusetts solar program, to take place the last week of October. Unfortunately, the procurement was delayed, and as a result, pricing uncertainty remains. This is because the initial SMART procurement will set prices for subsequent blocks. The Massachusetts Department of Energy Resources has now updated the schedule, and November 27 will be the opening date for bid applications, with mid-January as the date to release the results. Meanwhile, hearings took place last month to increase the state’s net metering cap, a constant legislative issue in Massachusetts.

- JEA, located in Jacksonville, Florida, has announced plans to procure nearly 300MW of solar. As we get closer to a federal investment tax credit (ITC) stepdown, expect more similar announcements from municipal utilities, coops, and investor owned utilities in 2018.

- An additional 1.2 gigawatts of solar projects were added to the PJM interconnection queue in Virginia, likely in response to Dominion's RFP announcement to procure 300MW (probably for Facebook).

- Our engineering team has been researching the wild, wild world of weather file selection, which is an important input for modeling the expected energy production of a solar project. There are a number of different public and private sources for this data, and the difference in solar radiation between different weather file sources for a single site can be up to 5%, no small margin. There are many factors to consider when choosing a weather file, and more nuanced research into the most appropriate weather file for a specific site may improve the value of projects.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered 650MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.