Friends, Clients, Customers Partners,

Each year we take a collective breath as a company to take stock of where we are and what’s happening around us. This year is no exception. Below, we share our thoughts on the current state of the solar market and Sol Systems. Take a look if you’d like, and feel free to follow up with us with any questions you may have.

The solar industry is thriving, but it remains a volatile place where new entrants and old ones struggle as they build, collapse, succeed, and fail - sometimes in that order. This past year was a turning point for the industry. The federal investment tax credit (ITC) was extended in full through 2019, and in part through 2023; a huge number of corporations have dedicated themselves to go 100% renewable energy and are procuring solar energy aggressively; and there are now over one million solar systems in the United States. At the same time, the single largest renewable energy developer filed for Chapter 11 bankruptcy protection; the two largest US manufacturers have lost over 50% of their value in the last 12 months; and the single largest residential developer and financier is struggling with financial difficulties. Still, the outlook is good, but realizing it is complex. Here’s our take.

The Transformation of the Energy Industry Means Competition

The energy industry is undergoing a fundamental transformation unseen since the mid-1930s when the United States provided millions with electricity throughout the Midwest through the Rural Electrification Act of 1938. Natural gas, solar and wind energy, and storage (basically in that order) are driving production, delivery and demand disruption, plus energy efficiency and more active customers are also contributing. Solar is quickly becoming one of the most competitive sources of electricity for corporate, industrial, and municipal users. But the solar industry is not alone.

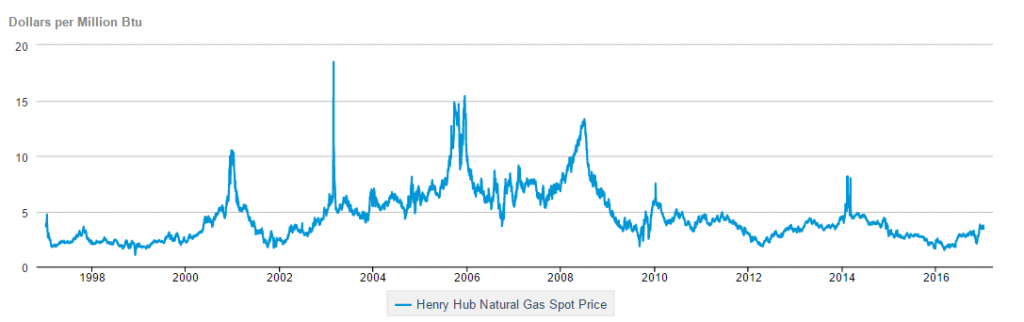

Huge U.S. natural gas discoveries in the last half decade, new technologies around hydraulic fracking and horizontal drilling, and new pipelines have brought all-in prices for natural gas down dramatically. Henry Hub pricing has fallen dramatically in the last decade and now stands where it did in 2008. But, today, most of the gas purchased in the United States is actually produced in the United States, and much of that gas is being used to produce electricity. In fact, for the first time in our history, natural gas produced more electricity than any other source in 2016. Natural gas pricing is set to be fairly stable in the next 3 years, and we expect that with coal plant closures it will continue to drive electricity pricing around the country.

Natural gas will cannibalize coal and nuclear power, and will compete directly with solar (especially large solar projects serving corporate customers and utilities). Solar will also compete with wind projects having increased hub heights, longer and more efficient blades, and cheaper turbines, not to mention a production tax credit (PTC) that provides almost sixty percent (60%) of the CapEx of wind projects. Coal, nuclear, and large-scale hydroelectric will fade as regulations, a stable electricity market, storage, and power plant fleet age catch up to existing assets.

So how can solar compete in this environment? We believe that solar succeeds in this highly competitive reason for 5 reasons:

- Solar costs are falling faster than any other technology – 20-40% each and every year for the last 10 years.

- Solar empowers stakeholders to engage in their energy procurement, financially support that technology, and vote for it. Each and every rooftop system helps solar build a political constituency that supports solar incentive programs and solar policy.

- Shorter development timelines than any other technology mean projects can scale up quickly to meet demand in specific regions. The electricity market is a volatile and dynamic market, and this flexibility favors solar when corporations are procuring solar, when utilities need to replace or develop electricity supply quickly, and when communities are concerned about carbon emissions. Solar projects can also be sized appropriately to a customer’s load, and solar can exist in suburban environments.

- Limited environmental issues compared with natural gas, hydro or even wind projects mean more community support. While wind maps point to restricted and specific areas, solar projects can produce electricity competitively in virtually every state in the country.

- Solar produces when energy is needed for the most part, which means it doesn’t disrupt energy markets like wind has done in Texas.

Deep Dive: Costs Will Continue to Decline

In 2010, I vividly remember sitting at my desk and hearing that modules were being sold at a then jaw-dropping $2/watt. That number was as unbelievably cheap at the time, and seems outlandishly expensive now. Projects at that time were being built for $4-5/watt. We expect to see module pricing at or around 40-45 cents/watt for conventional polysilicon modules, and drop below 40 cents in 2017. That’s a 20% reduction in just the last couple of months. Some are predicting solar modules in the 20-30 cent range by 2018.

Balance of system costs (such as racking, inverters, and installation) are all coming down in price. Single-axis trackers have become so cheap that they’ve become the industry standard for large systems in most markets. Chinese inverter manufacturers (inverters condition and transition a solar project’s DC electricity to AC) are reducing costs by 50%, producing inverters at 4-8 cents/watt. Additionally, new 1500 Volt dc applications used in Europe are now being integrated into U.S. projects, reducing cabling costs, installation time, and even system level energy losses. Simultaneously, the industry is just getting better at building solar, resulting in reduced labor costs per watt and overhead as well.

This downward pricing has put pressure on high efficiency modules produced by U.S. companies like SunPower and First Solar. Subsequently, their stocks have declined 49% and 72% respectively in the last 12 months. That makes solar look ugly from a public equities perspective, which is how most people consume information about solar. But, that’s a myopic view.

In fact, these price declines mean that solar projects can deliver energy at an increasingly competitive price. Our team estimates that for each 10 cent/kW decline in all-in pricing for utility solar projects, our industry can reduce power pricing by about .5 cents/kWh. That doesn’t sound like much. But, it means that if we can bring solar project pricing down by 30 cents in the next three years, we’ll bring power pricing down by 1.5 cents. That’s huge for a project selling power at 4-5 cents. Take a moment and consider what this industry can do in the next 10 years, or 20 years.

Simple steel in the ground and silicon in the sun, with minimal moving parts, mean a very attractive long-term energy asset with minimal production risk. Lower risk assets are lower risk investments, which is why large insurance companies like John Hancock and Prudential are doubling down on solar. Lower risk investments mean a broader pool of capital and a lower cost of capital, which means that solar owners can finance their systems long-term more readily, and offer energy customers lower energy pricing.

In short, solar will rapidly compete directly with wind and natural gas - which is one reason that corporates are procuring solar power directly.

Corporations Will Increasingly Control Energy Markets – and Buy Solar

Corporations are procuring energy directly from projects, either through physical delivery, or through “virtual” delivery via a contract for differences (CFD). In the last 18 months, General Motors signed a PPA for 34MW; Google, for 43MW; Amazon, for 150MW; Apple, for 130MW; Kaiser Permanente for 153MW, and Dow Chemical for 200MW. Over 500MW of solar have been built to serve corporate and municipal customers directly in the last two years.

Our advice for corporates entering into this market is that they must do their homework. Customers should consider the correlation between nodal or zonal pricing at their load node, and nodal pricing at the solar project; long-term congestion risk as other future power projects can depress nodal pricing; and development risks (double check development timelines, risks, and the bona fides of your developer partner). Corporates should also be aware of some of the accounting implications, namely derivative accounting, that are critical in Contract for Difference (CFD) transactions. Perhaps most importantly, we suggest that corporates think of offsite contracts as a hedge against volatility, and a tool for sustainability, rather than a tool to lock in savings. Energy prices go up and down, and sustainability officers would do well not to promise too much to their CFOs.

We believe we will see an explosion of corporate interest in offsite renewables, and specifically offsite solar. Most energy load is urban in nature, and rooftop solar cannot effectively offset enough of this load (we’re currently developing one of the most complex urban installs in history, and it is a challenge). Generally speaking, solar projects can be located closer to load (which reduces basis risk) and developed more quickly around a customer and their interest. Additionally, a distributed solar fleet that serves customers can be broken out and located throughout a RTO or ISO, which further reduces basis risk.

This is why we’re investing heavily in these assets with development partners, and also working closely with a number of corporate, educational, and municipal partners to help them achieve their sustainability goals.

Solar Scales

Solar employs hundreds of thousands of people in every state in this country including finance, construction, manufacturing, development, and asset management professionals. Solar has gone global, it has gone big, and it has gone corporate. There are certainly downsides to this growth, but we believe it is the natural maturation of an industry and one that we can all be proud of.

The result is that Southern Company, Sempra Energy, Dominion, Excel, Exelon, ConEdison, MidAmerican, and every single large energy company in this country is either developing solar assets or has invested in companies that develop solar assets. Goldman Sachs, JP Morgan, Bank of America, Wells Fargo, US Bank, PNC, M&T and virtually every large U.S. bank in the country has invested in solar projects. Google, Amazon, Microsoft, GM, Apple and hundreds of companies now purchase solar energy. We welcome them.

Development companies that would like to compete in the industry must find a niche, should ideally choose geographic focal points, and must focus to succeed. The notion that a developer has to be vertically integrated is slowly subsiding. New companies and old ones are providing high-quality service for solar developers to scale – namely highly efficient pure-play EPCs, niche engineering service, localized real estate experts, and sophisticated software that can displace inefficient manual efforts. We believe the runway for efficiencies is long, and we’ve yet to see the full maturation of the industry.

Companies that focus on specific niches such as community solar, like Clean Energy Collective and SunShare, or specific geographic markets, like Bluewave Capital or Borrego, will succeed. Too many have tried to be too many things for too many customers or stakeholders. It’s a challenge that some of the largest solar companies have worked through, or in some cases, failed to work through.

So What Are We Concerned About? Tax Reform

The federal investment tax credit (ITC) drives the entire solar industry and was extended recently through the active work of both Republicans and Democrats. The ITC provides a 30% tax credit for companies and individuals investing solar project through 2019, at which point it steps down each year to 10% in 2023. Pending tax reform raises two challenges. Banks, insurance companies and utilities are faced with significant uncertainty with respect to their actual tax rate (the corporate tax rate is currently 35%), and are concerned that the Administration tries to kill the ITC.

Our view is that an Administration focused on creating jobs and growing the economy will not take an axe to the ITC at such a critical stage in the industry’s development given the industry’s more than 200,000 jobs. We are more concerned that uncertainty around tax rates is slowing the entry of new investors. Companies account for (and value) infrastructure investments based depreciation schedules, capitalization policies, tax incentives, their tax rate, and their actual tax liabilities. With ambiguity around tax reform, and without a clear understanding of their tax obligations, banks, insurance companies, and utilities cannot effectively manage their investments. The one silver lining for solar is that the problem is even more acute for other tax incentives like the historic tax incentive, and potentially the federal production tax credit.

We think this risk is actually relatively benign, but the optics are the challenge. Our institutional clients have gotten comfortable with the fact that any tax reform is unlikely to impact 2017 tax liabilities, or even 2018 liabilities. Tax reform generally takes place over a number of years. Further, the Administration will not take aim at the ITC given its natural step-down and the industry’s jobs. Even if the ITC were reduced, such a change would be prospective, and would not impact current investments since the ITC is accounted for in the year the project is delivered. If you are considering making ITC investments, we encourage you to talk to our Fund & Asset Management Team.

And, How About Sol?

Amid this change, building a solar company is no easy feat. We’ve invested in people and an energy infrastructure that is dynamic in order to adjust to a fast-changing industry. Sol Systems efforts are best viewed through our three relatively independent operating units.

Our oldest business unit trades, aggregates, and finances environmental commodities on behalf of the company and thousands of customers. This company aims to vastly expand our solar renewable energy credit (SREC) financing program in 2017, and continue to expand into other environmental commodities, to assist our developer and customer partners. We expect to grow our customer base by 25MW in 2017.

We established what is now Sol Asset & Fund Management in 2012. That business unit manages hundreds of millions of dollars of solar assets on behalf of our institutional clients, and will increasingly be managing private funds that actually own solar assets on behalf of some of these clients. We currently asset manage over 300MW of solar assets. We expect to manage 440MW by the end of 2017 for this business line.

Finally, in 2015-16 we began working with select clients to develop solar assets for them. We refer to that team as Sol Development. We grew this team to one of the largest groups in the industry specifically focused on providing corporate customers with onsite and offsite solar procurement solutions. We expect to develop between 50-100MW of solar projects on behalf of these customers in 2017.

In Sum….

We’re proud of the evolution of our businesses, optimistic about the future of Sol (and our industry), and indebted to a team that has made this incredibly exciting journey a reality. And mostly, we’re indebted to many of you for being our partners, our clients, and our friends. Thank you. Our joint commitment and hard work drive the positive change in this world we endeavor to craft.

Yuri