In early 2016, Massachusetts hit its SREC II program cap and had many in the solar industry asking: what’s next for the Bay State? To help answer this question, the Massachusetts Department of Energy Resources (DOER) issued SREC II extensions and then an initial outline for the new Solar Massachusetts Renewable Target (SMART) Program in January of 2017. The initial outline confirmed that there would not be another SREC program, but rather a tariff-based incentive program. The draft design for the program was announced on June 5, 2017. On August 25, 2017, the DOER filed the final version of 225 CMR 20.00 with the Secretary of the Commonwealth’s office.

From Start to Finish: What Changed?

Much of the initially proposed mechanics of the program are still in place with slight variances in the final version. SMART will lock projects into fixed-rate contracts for either 10-year or 20-year terms. Projects ≤25kW will be locked into 10-year contracts, and projects >25kW will be locked into 20-year contracts. The program aims to award these fixed-rate contracts to a total of 1600MWAC of projects. This capacity will be allocated among eight 200MW blocks, and apportioned by the electrical distribution companies’ (EDCs) share of 2016 total electric load. An initial 100MW procurement for projects sized 1-5MW will be used to determine the Base Compensation Rate for these blocks, and from there the Base Compensation Rate will decline 4 percent per block.

While the overarching design is still the same, the most recent round of regulations revealed changes to the initial procurement and how the Base Compensation Rate will be determined. The initial procurement will now have a bid-price ceiling of $0.17/kWh rather than a $0.15/kWh price ceiling for projects 1-2MW and a $0.14/kWh price celling for projects 2-5MW. Rather than the clearing price, which is equal to the highest requested Base Compensation Rate, to set the program’s initial Base Compensation Rate, the rate for the first block of capacity will now be a calculated mean price of all proposals selected in a Distribution Company’s service territory.

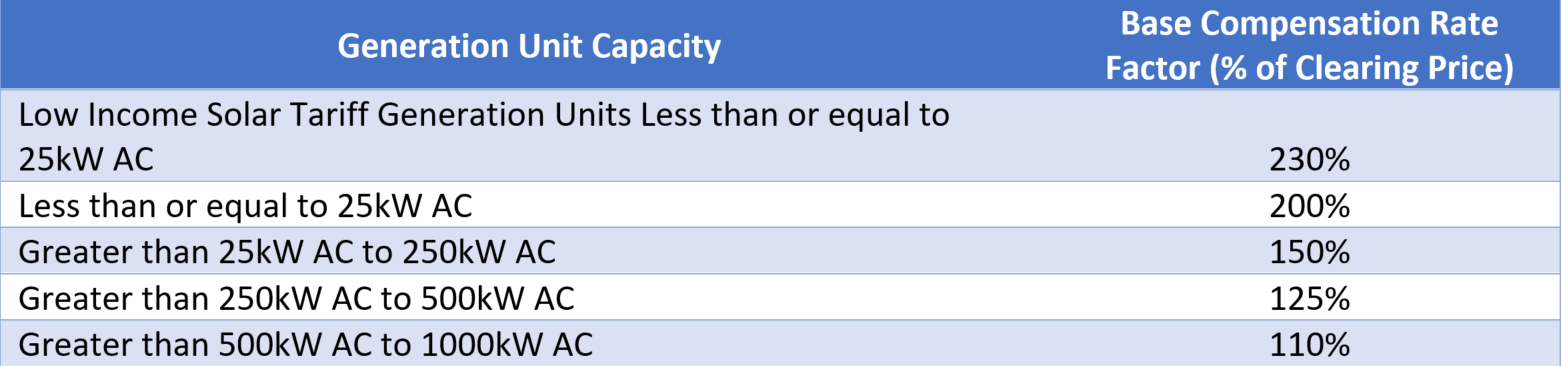

While calculations for the Base Compensation Rate changed, rate factors for systems under 1MW stayed the same and are shown below:

For systems greater than 1MW, per kWh compensation rate adders will be available based on location, off-taker, and technology to encourage the use of storage and trackers. A project can use up to one adder in each category to further supplement its Base Compensation Rate. While the initial rules placed a 320MW cap on adders available under the program this was removed under the final rules. DOER has instead established 80MW tranches of capacity for adders, and adders will decline by 4% with each tranche. The most significant adders for the locational-based adder category are for carports, and offer an additional $0.06/kWh. Combined with rooftop adders of $0.02/kWh, it’s clear that the Commonwealth aims to incentivize under-utilized spaces such as roofs and surface parking lots.

In contrast, the state is disincentivizing developers from utilizing large, open spaces, especially agricultural land. For systems larger than 500kW, subtractors to the Base Compensation Rate will come into play if the projects are classified as Category 2 or Category 3. These subtractors will range from $0.001-$0.0005/kWh per acre of land based on the acreage covered by the modules themselves. This is meant to push the Massachusetts market away from greenfield development and towards building and brownfield-sited projects. However, under the final rules, exemptions from subtractors were added for systems that had all necessary qualification documents obtained by June 5, 2017 or can demonstrate a good cause for exception.

These adders and subtractors will still be incorporated via the same formula:

𝑆𝑜𝑙𝑎𝑟 𝐼𝑛𝑐𝑒𝑛𝑡𝑖𝑣𝑒 𝑃𝑎𝑦𝑚𝑒𝑛𝑡 = (𝐵𝑎𝑠𝑒 𝐶𝑜𝑚𝑝𝑒𝑛𝑠𝑎𝑡𝑖𝑜𝑛 𝑅𝑎𝑡𝑒 + 𝐶𝑜𝑚𝑝𝑒𝑛𝑠𝑎𝑡𝑖𝑜𝑛 𝑅𝑎𝑡𝑒 𝐴𝑑𝑑𝑒𝑟𝑠 − 𝐺𝑟𝑒𝑒𝑛𝑓𝑖𝑒𝑙𝑑 𝑆𝑢𝑏𝑡𝑟𝑎𝑐𝑡𝑜𝑟) ∗ 𝑡𝑜𝑡𝑎𝑙 𝑘𝑊ℎ 𝑔𝑒𝑛𝑒𝑟𝑎𝑡𝑒𝑑 − 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑒𝑛𝑒𝑟𝑔𝑦 𝑔𝑒𝑛𝑒𝑟𝑎𝑡𝑒𝑑

Another change made from the initial filing to August’s final version includes a 35 percent cap placed on systems less than or equal to 25kW per block with a 20 percent minimum. Additionally, the removal of onerous restrictions for qualification as an Agricultural Solar Tariff Generation Units were eased and will be replaced with still-to-come guidelines that will need to be complied with. Improvements were also made to restrictions placed on the usage of continuous parcels, as well as the usage of multiple parcels for one project and each of these are now allowed under specific circumstances.

One key piece still missing from the most recent release of SMART rules, is a clear path for the Alternative On-Bill Credit. This lack of clarity is exacerbated by the fact that net energy metering (NEM) caps have, for the most part, been hit in National Grid, Eversource, and WMECO territories. Seeing as SMART’s On-Bill Credit mechanism may supplant NEM, further details on the matter are anxiously awaited.

End of an Era and New Beginnings

Though final rules have been announced, the biggest question surrounding SMART remains. When will the SMART program officially begin? Based on the next steps needed by the Department of Public Utilities (DPU), mid-2018 seems likely. Utilities must file tariff proposals with the DPU by the end of September, and will have to develop auction materials by October 24th. The initial procurement to set the Base Compensation Rate, will then likely occur the last week of October and will be announced by end of December. In addition to DPU actions, a third party administrator for the program needs to be selected. This should be done by April 2018. Finally, tariffs will be finalized between May and June 2018 which is when incentive dollars will start to flow.

So, there is still time before SMART officially kicks off; however, this doesn’t mean the market must pause during the transition. There is still space under SREC II to get projects registered until SMART is implemented, and Sol Systems is here to help you get it done. Please email us at info@solsystems.com to learn more.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered more than 600MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.