Whether tis nobler in the model to suffer / the cost and hassle of outrageous procurement expense…

As the clock ticks into the third quarter of the year, solar energy developers are increasingly confronted with a question of Shakespearean proportions: in order to preserve 4 percent additional investment tax credits (ITCs) on a project prior to the step-down in 2020, is it worth the cost and friction to take steps to incur 5 percent or more of project costs in 2019? While the mindset of the typical solar professional will be, of course, to maximize all possible benefits, it is worth pausing to consider the complexities involved in safe harboring via equipment purchases and weigh some situations when less is in fact more.

Setting the Stage

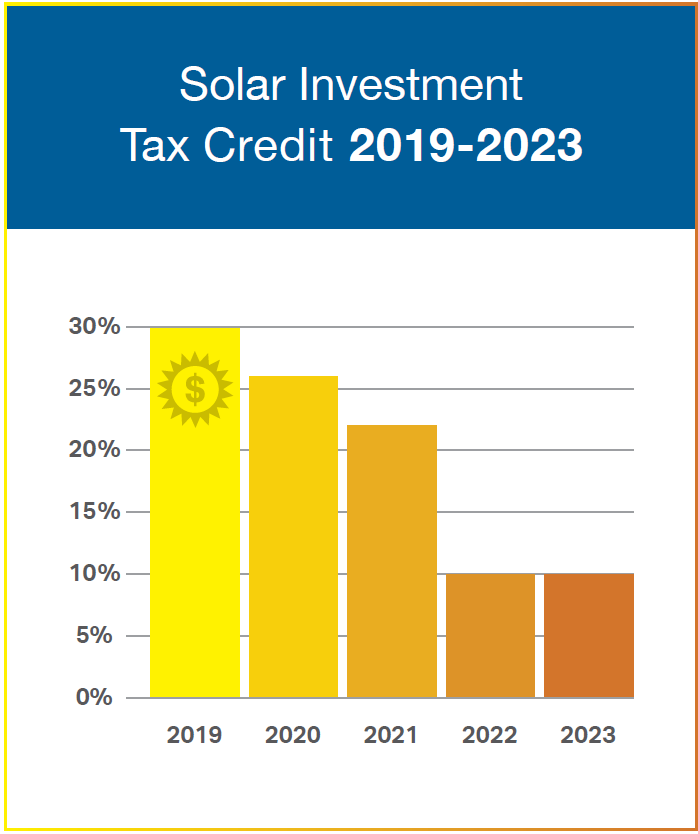

At the end of 2015, Congress passed an ITC extension and gradual step-down beginning in 2020, decreasing 4 percent per year before dropping to 10 percent in 2022 for commercial systems (or zero percent for residential). Projects will qualify for the ITC percentage in the year in which the project commences construction, and two paths are provided for meeting this standard.

At the end of 2015, Congress passed an ITC extension and gradual step-down beginning in 2020, decreasing 4 percent per year before dropping to 10 percent in 2022 for commercial systems (or zero percent for residential). Projects will qualify for the ITC percentage in the year in which the project commences construction, and two paths are provided for meeting this standard.

First, and most logically, a project can qualify by commencing “physical work of a significant nature.” However, solar projects that have not been fully permitted or are not fully financed may not have this option. In that case, a second path is available to meet the “commence construction” standard: incur at least 5 percent of the total depreciable cost of the system in the given year, otherwise called “safe harboring.” The upside to this approach is that a project then has until the year 2024 to place in service and still maintain eligibility for the 30 percent credit. While the second path is technically simpler – it does not require activity on the site and could even be applied to projects that do not have a specific site yet identified – it forces a project developer to confront a series of meaningful assumptions.

Yet There Is Method In’t

First and foremost, expending 5 percent of a system’s total cost before financing is secured requires, well, money. More to the point, it requires access to a large balance sheet, development capital, or early construction financing tolerant of financing risk in order to make the investment. Not all project developers are blessed with large parent companies or understanding lenders. Simply determining if funds can be accessed for the purpose is often the first gating question for safe harboring a project.

The next consideration is an obvious one – 5 percent of a project’s cost must be spent, but on what? Because design work is likely not advanced enough to make procurement decisions for racking or inverters, modules are the obvious choice. While racking and inverter orders will be specific to a project’s final design, and in the case of inverters, may require utility approval, modules can be reliably integrated into a project regardless of where the final design shakes out. Just buy enough modules to exceed 5 percent of total project cost (and make sure to leave some buffer, should project size or costs unexpectedly increase) and you’re done – right? Well, perhaps. A few additional considerations must be made.

First, depending on the facts and circumstances relevant to a project owner’s accounting election, it is likely necessary to take delivery well in advance of equipment deployment and thus incur storage costs for that equipment. Costs for storing equipment (climate controlled and insured, of course) could total $0.03 per watt per year. Safe harboring modules also requires buying equipment in two separate batches months or even years apart, creating a scenario where the same module may not be available.

This second consideration is more difficult to quantify. Buying mismatched modules makes engineering more challenging and could even decrease a project’s value through production constraints. A third consideration is simple economics – module prices are currently quite high due to tariffs but also in large part to a tight market thanks to growing global demand and, ironically, this very rush to safe harbor equipment. Expending 5 percent of project costs on modules equates to around a third of a project’s total module purchase. Falling module prices over the next 12-18 months could erode some or all of the value of the 4 percent ITC preserved by safe harboring, if the developer could have alternatively purchased a large portion of the project’s modules at a lower value.

Finally, and not insignificantly, developers running a lean shop must consider if the burden on operations to analyze, bid out, finance, purchase, and store equipment in order to successfully safe harbor (not to mention the requisite legal opinions) is really worth the potential benefit. Even the most ambitious solar professional must acknowledge that one can only complete so many deals in a year – and the lift to successfully put in place a safe harboring program for a portfolio of assets is easily on par with the brain damage necessary to execute a complex purchase agreement or fund financing. If a company decides to prioritize safe harbor efforts, what other opportunities must be overlooked or compromised?

Ultimately, the question of whether to safe harbor comes down to a cost-benefit analysis. A project owner financing safe harbor procurement can and should look at a full financial model to consider factors around construction spend and timing, tax equity financing terms, and cost of capital to procure equipment early. For a developer planning to sell an asset but desiring to preserve 30 percent ITC value, however, this analysis can be very simple.

There is Nothing Good or Bad, But Thinking Makes It So

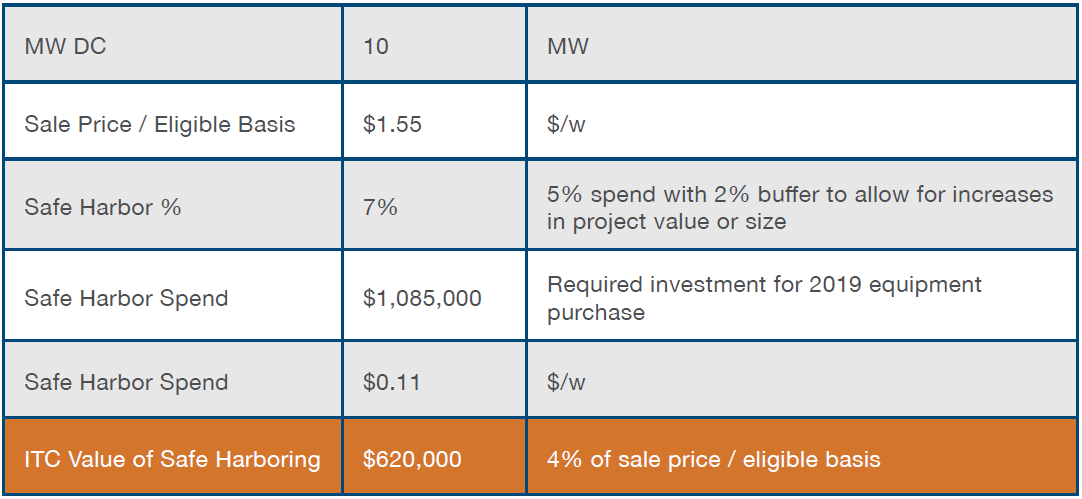

Let’s assume a 10MW project that costs $1.05/W to build can be valued for $1.55/W in a 26 percent ITC world. For simplicity’s sake, we will assume that $1.55/W is also the portion of the system that qualifies for five year accelerated depreciation, and thus forms the denominator of the 5 percent safe harbor calculation. If the developer can successfully safe harbor the system at a 30 percent ITC, they unlock an additional cash-on-cash value of $620,000, or 4 percent of $1.55/W, on a simple return on investment basis. Sounds like a no brainer, right? Well, let’s take a closer look.

To Safe Harbor...

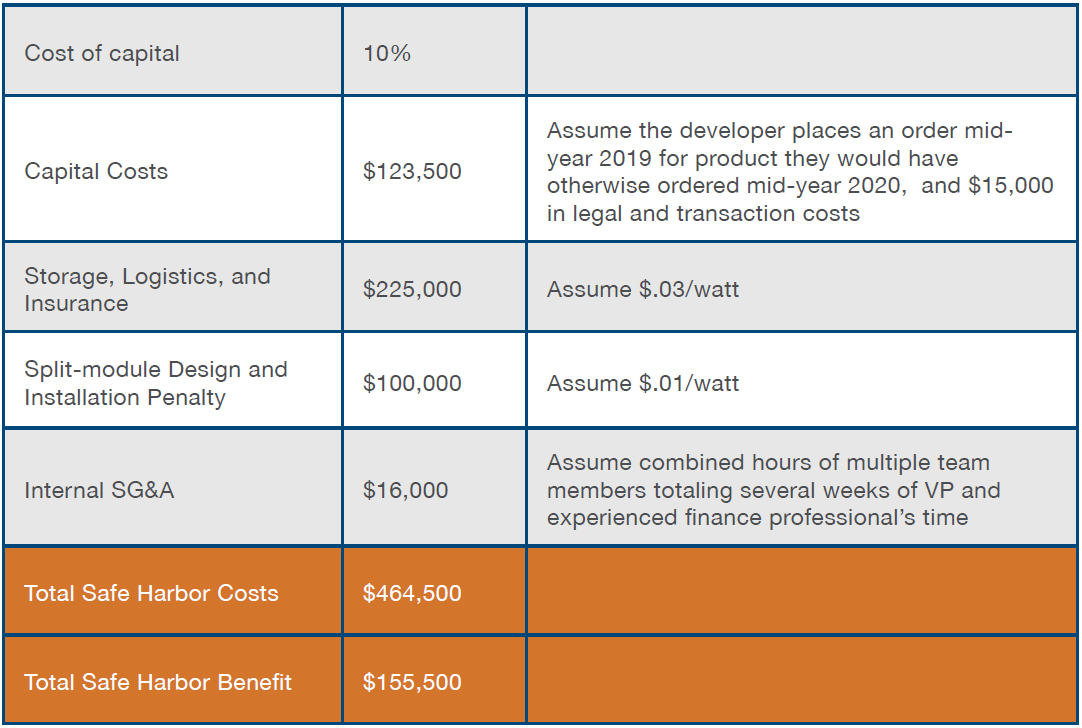

This developer is going to assume a buffer of 2 percent on top of the 5 percent safe harbor requirement. After all, there would be nothing worse than putting in the effort to safe harbor the system, only to find out that the project size or depreciable cost increased enough to fail to qualify for the safe harbor, or force the developer to downsize the project. That means the developer must spend $1.085mm, or 7 percent of $1.55/W, to meet the safe harbor threshold. Let’s also assume the equipment must be purchased right about now given delivery timelines and increasingly tight supply as manufacturers sell out their capacity in the rush to safe harbor. And the developer won’t be paid the bulk of their construction costs for a full calendar year. Assuming a rather fair cost of capital of 10 percent, the developer will incur $108,500 of interest expense/carrying cost, plus closing costs, opinions, and fees of, say, $15,000, for a total capital cost of $123,500.

And assuming the equipment arrives year-end 2019 and cannot be deployed until the fall of 2020, the developer will have to price in at least three-quarters of a year of storage, insurance, and additional delivery costs. At $0.03/W, that’s another $225,000 of safe harbor costs. If the developer is not able to procure the same type of module and costs increase due to complexity of design, or if the developer pays a premium to obtain the same module as originally purchased, they may pay an additional cost – let’s say $0.01/W, or $100,000. Finally, we’ll make a consideration for the time and overhead incurred by this developer if professionals from their finance, engineering, and executive teams dedicate hours totaling several weeks on this endeavor – say, $16,000 total.

The argument for safe harboring does not appear quite so strong after a quick accounting of the costs involved. The overall expected benefit of $650,000 must be reduced by costs of just under $465,000, reducing total potential upside to $155,000. Was that really worth the hassle?

Or not to Safe Harbor...

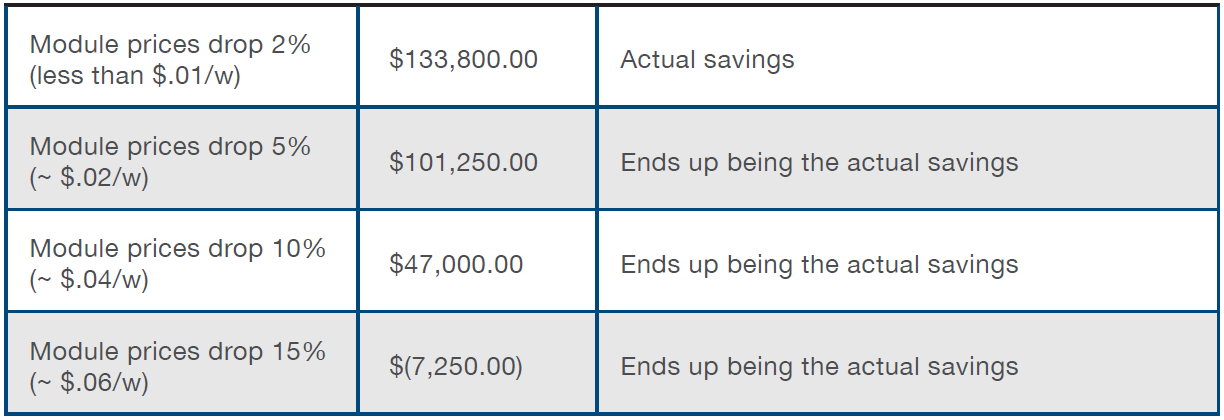

Still, the benefit may be there for a developer, especially one with a robust team and significant pipeline sufficient to justify the effort – save for one factor. Critically, module prices are unusually and unjustifiably high. We know that availability is limited due to a rush to safe harbor, global market dynamics affecting price and availability, and tariffs driving prices up further. It is highly likely prices will fall in the period between the purchase of safe harbor equipment and the point at which that equipment would normally have been purchased for that project. In fact, in this scenario, module prices would only have to drop by 15 percent to completely erode the safe harbor benefits so hard won by the developer’s efforts. Any additional efficiency gains in modules on the market one year from today, either due to pure yield gains or balance-of-systems efficiencies from increases in module power class would further increase this gap.

Erosion in Benefit

To Thine Own Self Be True

In the end, the decision of whether or not to safe harbor will be a highly individualized one specific to each project and developer. Obviously, valuing the project on the basis of internal rate of return that accounts for the time value of money of ITCs received in the first year of an investment will show more benefit than an ROI view. Certain advantages related to cost of capital, procurement or storage terms, and the overall ease and speed at which a developer can put these measures in place may greatly improve the cost-benefit analysis. We simply make the case above to illustrate that safe harboring for a project is by no means a foregone conclusion, or even necessarily a net benefit on an ROI basis. Often the hardest decisions made on a project are those to forego an opportunity to maximize benefit, since the one constraint we can apply to all projects with certainty is the number of hours in a day. The question for solar developers is how to use them.

This is an excerpt from the Q2 2019 edition of The SOL SOURCE, a quarterly electronic newsletter analyzing the latest trends in renewable energy development and investment based on our unique position in the solar industry. To receive future editions of the journal, please subscribe.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008.

Over the last 11 years, Sol Systems has delivered 800 MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com