The Sol SOURCE is a monthly journal that our team distributes to our network of clients and solar stakeholders. Our newsletter contains energy statistics from current real-life renewables projects, trends, and observations gained through monthly interviews with our team, and it incorporates news from a variety of industry resources.

Below, we have included excerpts from the June 2017 edition. To receive future Journals, please subscribe or email pr@solsystems.com.

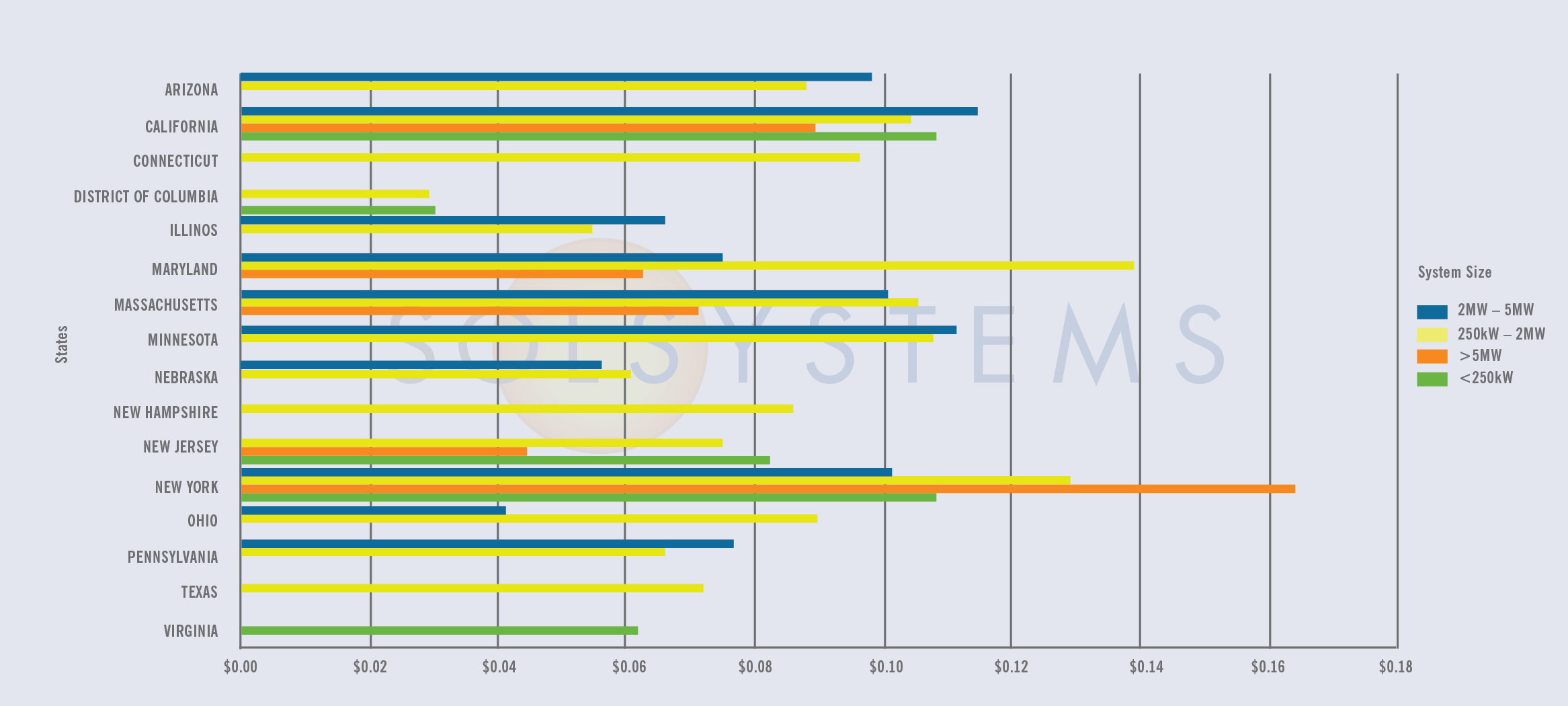

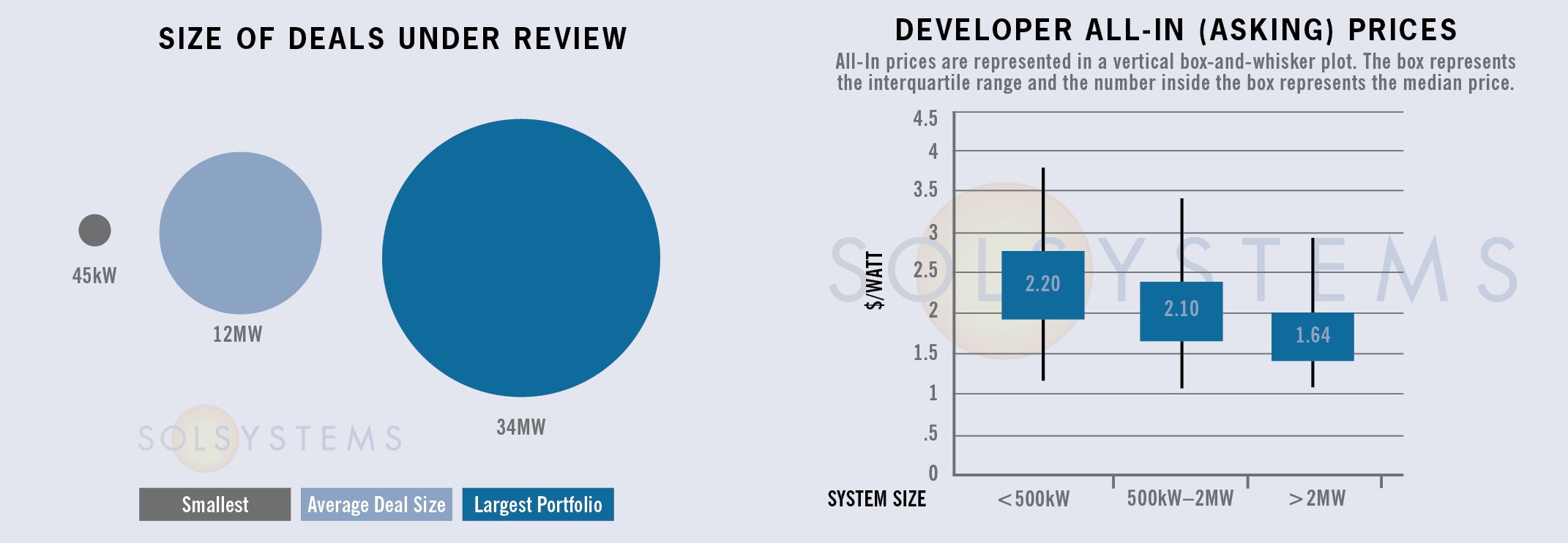

PROJECT FINANCE STATISTICS

The following statistics represent some high-quality solar projects and portfolios that we are actively reviewing for investment.

Have a solar project in need of financing? Our team can provide a pricing quote for you here.

STATE MARKETS

California: It’s baaaaaaaaaaaack. After a multi-year hiatus, the Los Angeles Department of Water & Power (LAWDP) has announced the latest iteration of its solar feed-in tariff program. The program will span 65MW, and of that, 35MW will be procured at a fixed price of 14.5 cents/kWh, and the other 30MW will be in competitively priced blocks. LADWP expects the program to open later in the month, and more information can be found here.

Developers interested in financing for California solar projects can reach out to Anna Noucas (anna.noucas@solsystems.com), our West Cost Origination Lead based in Southern California. We’d be happy to help.

Illinois: The Future is here! June 1 marked the effective date of the Future Energy Jobs Act (FEJA), the Land of Lincoln’s landmark renewable energy law that could generate as much as 1.35GW of community solar, distributed generation, and utility-scale solar by 2020. First comes law, then comes implementation. In late May, the Illinois Power Agency hosted a series of workshops to discuss outstanding program design issues for the initial utility-scale (>2MW) procurement, community solar, and the Adjustable Block incentive program (projects <2MW). The first RFP for utility-scale solar (and wind, for those watching) will be released on June 28.

Notably, an estimated 400MW of community solar could come online by 2030 under FEJA. Unlike other community solar markets like Maryland, D.C., New York, and California which have been slow to get off the ground, the Illinois community solar market could be very promising. This is thanks largely to the flexibility that the statute provides the Illinois Power Agency to implement the program’s rules. For example, only three subscribers are required, but outside of that, the IPA has the discretion to decide rules for co-location, geographic diversity, and how a program may be treated differently (if at all) for having residential vs. mostly commercial subscribers. In this way, it is up to the Illinois Power Agency to pull from best practices from other states to ensure maximum megawatt deployment. Initial comments are due on June 27, and a draft Long-Term Procurement Plan will be filed later in the year for further comment.

Massachusetts: At long last, the Massachusetts Department of Energy Resources (DOER) filed its draft rules for SMART, the 1,600MW successor program to the Commonwealth’s successful SREC II program. Given delays stemming from SMART’s complexity, SREC II was extended earlier this year. With this release, solar advocates breathed a sigh of relief and are now beginning to draft their public comments, which are due July 11th. As for the DOER, we hope they are off somewhere on a well-deserved vacation before the flood of feedback comes in; the DOER will host listening sessions on July 10th and 11th.

We expect for SMART to officially open for business in summer 2018, and SREC II will be in place before that…if a project can get a net metering cap allocation. While National Grid’s private sector net metering cap has been hit for quite some time, public sector projects only recently hit their caps in NGrid territory. Net metering cap legislation will be heard in the state house this fall and provide the industry with some hope.

For a full summary on SMART, check out our blog.

SOLAR CHATTER

- Watt an accomplishment! Average utility-scale solar prices have dropped below $1/Watt for the first time ever in a Q1 that saw 1GW of utility-scale solar installed.

- Make room! Wind and solar now account for 10 percent of electricity generated in the US according to the EIA’s monthly power report for March. This is the first time the energy sources have reached this milestone, and the percentage is expected to continue its growth in the coming years.

- The Suniva case is real, and there is certainly cause for concern, with SEIA reporting that the tariffs sought in the case will cost the industry 88,000 jobs. The fight against the case continues for the industry, and the uncertainty it will bring will be hard to ignore in the coming months.

- What happens in Vegas…can now be sold back to the grid again. Nevada Governor Brian Sandoval signed a bill reinstating net metering for rooftop solar in the state after an 18-month hiatus that cost the state 2,600 jobs, many of which are expected to return with the policy. Sunrun, Tesla, and Vivint will all return to the market. However, shortly after, the Governor sent mixed signals by vetoing community solar and a more aggressive renewable energy standard.

- Despite the decision by the Trump administration to pull out of the Paris Climate Accords, renewable energy is showing its resiliency. Corporations are still setting high sustainability goals, with 900 American companies signing the “We are still in” pledge, affirming their dedication to curbing emissions regardless of the country’s position in the Paris agreement. Companies like Anheuser-Busch InBev have drastically increased their renewables goals recently, with the brewing company in particular setting out to generate 100 percent of their energy from renewables by 2025. Our policy team is also participating in more 50% renewable portfolio standard discussions in various state markets; stay tuned for SOURCE on more details in the coming months.

- Amid whispers we’re hearing of developers wanting to break into the Florida market, Governor Rick Scott signed Amendment 4 into law this week, which will exempt 80% of commercial solar installations’ value from the tangible personal property tax, as well as real property taxes for commercial properties. As we’ve discussed before, property taxes can be taxing, and this bill, according to SEIA, will help turn the Sunshine State into a “solar star.”

- North Carolina’s energy reform bill passed the house overwhelmingly and is now onto the senate. The bill, backed by Duke Energy, will shorten solar contracts, create a competitive bidding process for projects, and allow customers to purchase power from community solar farms, among other changes.

- Solar getting sporty! Here in D.C., the Verizon Center, home to Washington’s NBA, NHL and WNBA teams agreed to an offsite solar purchase that will power 25 percent of its operations with solar. Now we just need somebody to get the NBA’s Phoenix Suns on the line and explain to them the marketing opportunity.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered more than 600MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.