The Sol SOURCE is a monthly journal that our team distributes to our network of clients and solar stakeholders. Our newsletter contains energy statistics from current real-life renewables projects, trends, and observations gained through monthly interviews with our team, and it incorporates news from a variety of industry resources.

Below, we have included excerpts from the December 2017 edition. To receive future Journals, please subscribe or email pr@solsystems.com.

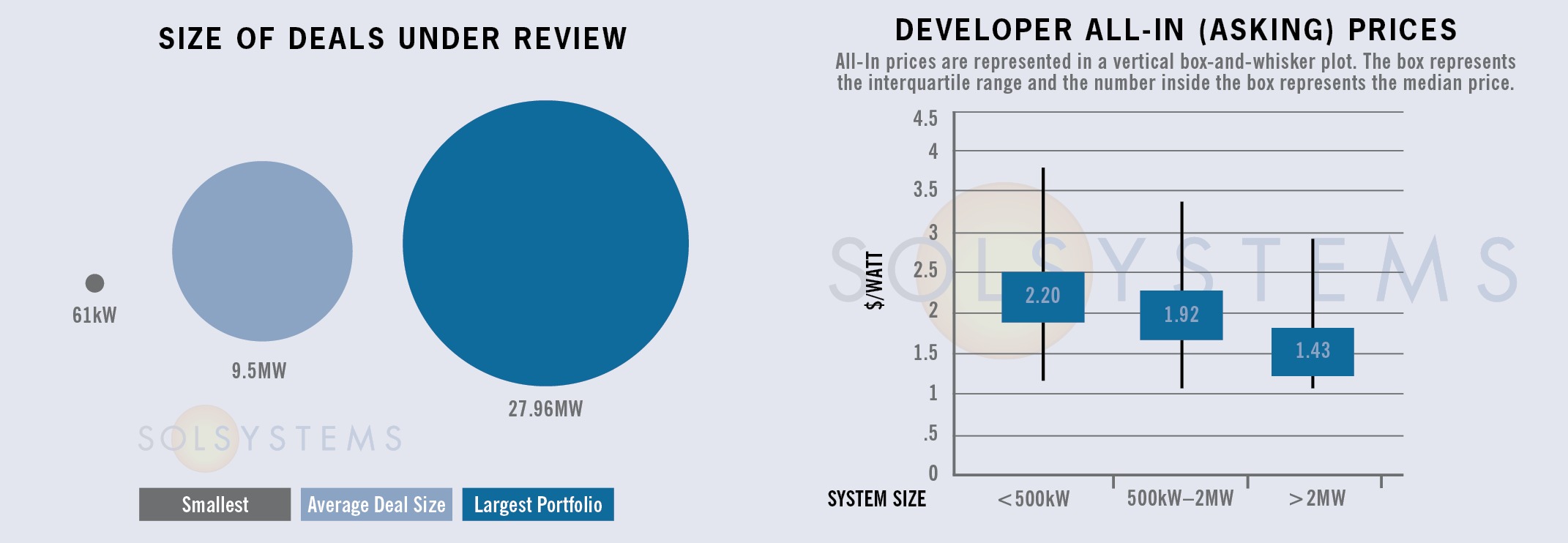

PROJECT FINANCE STATISTICS

The following statistics represent some high-quality solar projects and portfolios that we are actively reviewing for investment.

STATE MARKETS

Illinois –The Future Energy Jobs Act (FEJA) turned one this month. To celebrate, the Illinois Power Agency (IPA) released the latest iteration of its Long-Term Renewable Resources Procurement Plan (for a refresher on the first draft, check out the October issue of SOURCE). The Plan details the Land of Lincoln’s emerging community solar, rooftop solar (commercial customers up to 2MW are eligible), utility-scale solar, and low income solar and workforce training programs.

With the Long-Term Renewables Resources Procurement Plan, the Illinois Power Agency demonstrates how smart incentive design should be done. IPA used a transparent, public pro forma, soliciting public input for each key project variable. We think a key variable or two were missed in the latest draft (we’ve missed a MWdc / MWac conversion once ourselves, no judgment), but we are confident that these minor tweaks will be resolved prior to program launch, creating a top 2018 market.

The plan, filed with the Commission on December 4, and final objections are due on December 18th. After that, the Commission has an April 3, 2018 deadline for issuing an Order confirming or modifying the plan. With a few months necessary after Commission approval to It is still feasible to accept a late summer 2018 launch.

Illinois solar customers, get ready!

Massachusetts – More public agencies have caught onto the opportunity to lease unused land for the upcoming SMART program. Sol Systems expects that this program will be less focused on PPAs and behind-the-meter solar projects, and more focused onsite leases that are less complicated for customers. In this way, a customer will earn contracted revenue instead of using a PPA, which is focused on modeling projected savings. Additionally, the Commonwealth’s social goals have the industry moving solar projects from unused greenfield land to the built environment. Increased incentives make carports especially attractive under SMART. Property owners with large parking lots for solar canopies can contact us at anna.noucas@solsystems.com for more information about opportunities under this program.

Massachusetts has issued their RFP for the first competitive solicitation under SMART, which will set pricing for the program; bids were due on December 5. Results should be announced in mid-January, at which point customers will benefit from more pricing certainty.

New York – As we predicted, the New York State Energy Research and Development Authority (NYSERDA) is in early stages to reform its Megawatt Block program for commercial and industrial (C&I) solar. As a first step, they hosted a webinar in which they recognized that they are aware that rooftop C&I is not happening in the state, but that they would like it to. While the will may be there to revamp the program, one specific problem will be that projects that have already applied to the incumbent regime will not be able to reapply. Even with a “fixed” program, this could lead to a sluggish start for a revamped Megawatt Block.

This will be a critical development to watch in the coming months, and industry participation will be critical. The political will has certainly been there under the leadership of Governor Cuomo, but execution has been challenging, specifically as it relates to C&I rooftop solar with complex regulatory schemes such as the value of distributed energy resources (VDER) and some initial flaws with the Megawatt Block program.

We’re optimistic about this critical first step that NYSERDA is taken, and hopeful that New York may soon live up to its potential as a national clean energy leader.

SOLAR CHATTER

- The non-residential solar market (which we typically refer to as the “commercial” market in SOURCE) experienced strong growth this last quarter, according to the U.S. Solar Market Insight Report of Q4 2017. According to GTM Research and the Solar Energy Industries Association (SEIA), non-residential grew 22 percent year-over-year, largely due to a rush to finish projects by certain policy deadlines. Which policy deadlines? We’d say the Value of Distributed Energy Resources (VDER) in New York, the SREC II to SMART transition in Massachusetts, and changes to TOU rates and peak hours in California, to name a few.

- Rumor has it that a certain bankrupt module manufacturer that has caused quite a stir this year (to say the least) is trying to get itself sold to a more reputable company. Stay tuned; the rumor mill is buzzing.

- Climate change has had an unexpected effect on solar development this last quarter, at least from a delivery perspective. Hurricanes Harvey and Irma resulted in a shortage of electrical infrastructure equipment (such as components for switchgear), which has required some scrambling to secure project equipment.

- Passivated emitter rear contact (PERC) cells continue to dominate new model releases in the solar module market, and appears that they will for the next several years. At the same time, mainstream module manufacturers are also taking up more aggressive module architectures to improve efficiency, such as half-cut cells, bifacial modules, and wired busbars instead of ribbons. These are all helping to push efficiency, but as always, new technology can bring along new risks that must be assessed for investors.

- Will New Jersey soon follow Illinois and New York and become the latest state to offer zero emissions credits (ZEC) for nuclear power? Given the lack of public evidence that nuclear facilities are indeed failing in New Jersey, this legislation has been controversial; similar legislation earlier in the year failed to move. Nonetheless, this could be important to watch before Governor Christie leaves office. Regardless of what happens in the rest of 2017, one thing is for certain: 2018 is shaping up to be an interesting year in energy for the state of New Jersey. With the election of Governor Phil Murphy and plans to kick off a new Energy Master Plan, New Jersey can regain its place as a top East Coast solar market for years to come.

ABOUT SOL SYSTEMS

Sol Systems, a national solar finance and development firm, delivers sophisticated, customized services for institutional, corporate, and municipal customers. Sol is employee-owned, and has been profitable since inception in 2008. Sol is backed by Sempra Energy, a $25+ billion energy company.

Over the last eight years, Sol Systems has delivered 650MW of solar projects for Fortune 100 companies, municipalities, universities, churches, and small businesses. Sol now manages over $650 million in solar energy assets for utilities, banks, and Fortune 500 companies.

Inc. 5000 recognized Sol Systems in its annual list of the nation’s fastest-growing private companies for four consecutive years. For more information, please visit www.solsystems.com.